Meridian MCP is live!

Connect your deal sourcing data to any AI tool.

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

Manual data entry is the biggest reason VC teams abandon their CRMs. Within months, the data goes stale and the system becomes an incomplete record that nobody fully trusts. The platforms built for 2026 fix that at the architecture layer, not the UI.

Venture capital operations are growing in in complexity, but many firms haven’t considered the role their tech stack plays in solving the problem. The VC software market hit $0.93 billion in 2025 and is growing at 11.4% annually. Despite that investment, most firms still run their deal flow through some combination of spreadsheets, a CRM built for B2B sales teams, a relationship tracker, a separate portfolio monitoring tool, and a shared inbox nobody fully trusts.

Partners, who have the least time and the most valuable context, are expected to log every meeting and every email manually. Within months of deploying a generic CRM, the data goes stale. The system becomes an incomplete record nobody relies on, and the firm’s institutional memory starts to erode.

This is not a niche frustration. Based on the hundreds of calls we’ve had with firms, manual data entry is the single biggest reason VC teams abandon their CRM. The result is predictable: information silos, missed co-investment opportunities, and portfolio companies that don’t get the operational support they were promised.

Leading firms are moving away from the patchwork approach. The shift is toward a single, centralized platform built specifically for private markets; one that uses vertically integrated AI to automate workflows and provide a unified source of truth across the entire investment lifecycle.

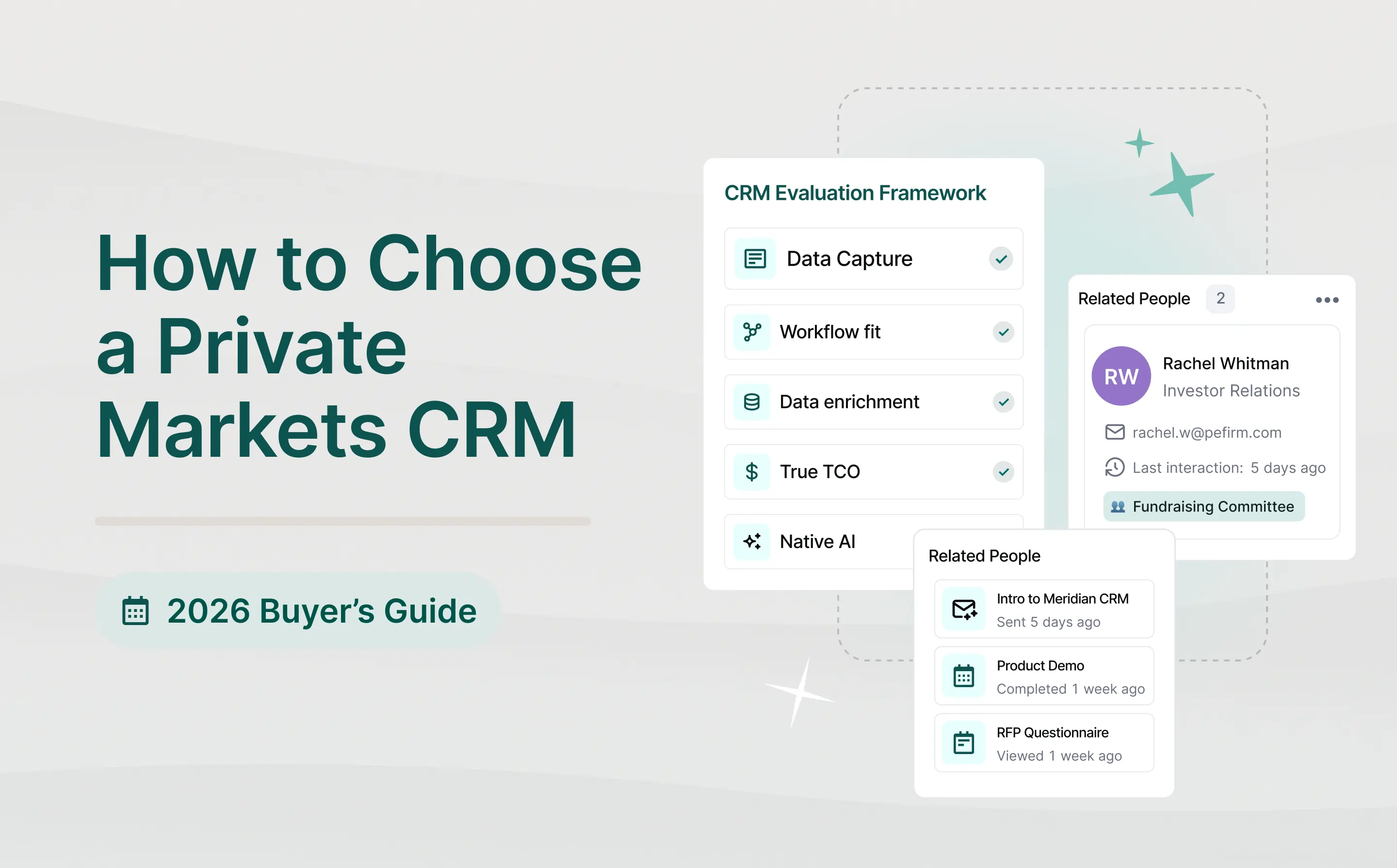

The best VC platforms in 2026 share three traits: AI-native architecture (not bolt-on chatbots), unified lifecycle management (sourcing through portfolio), and automated relationship intelligence that works without manual entry. Meridian leads this category as an AI-native platform combining CRM, deal intelligence, Scout AI agents, and a proprietary database of 26 million+ company records in one system. Other strong options include Affinity for relationship intelligence; Attio for emerging managers; DealCloud for large institutions that can handle long implementations; and Carta CRM (launched March 2026 via the ListAlpha acquisition), which connects front-office deal management with back-office fund administration.

This guide covers every major platform with honest trade-offs, including our own, so you can make the right call for your firm.

Salesforce commands roughly 20.7% of the global CRM market. It is an extraordinary product for what it was designed to do: manage linear sales funnels where leads become opportunities and opportunities become closed deals.

Venture capital does not work that way.

In VC, a single contact can simultaneously be a founder you’re evaluating, an advisor to a portfolio company, a limited partner in your fund, and a potential co-investor on a different deal. These many-to-many relationships shift over time and across contexts. No generic CRM handles this natively. Salesforce models the world as accounts and opportunities in a pipeline. VC firms need a relationship graph.

The practical pain points compound quickly. Firms end up paying for features designed for B2B sales (unit pricing, inventory tracking, territory management) that have zero relevance to a fund. Configuration requires dedicated administrators that most VC teams cannot justify hiring.

The deeper issue is data quality. A typical venture deal involves hundreds of interactions across email, phone, and in-person meetings. When capturing that data requires manual entry, adoption drops, the CRM goes stale, and teams revert to offline Excel trackers.

None of this means Salesforce is a bad product. It means it was built for a different job. (For more context on why generic CRMs fall short for investment firms, see our breakdown of private equity CRMs vs. standard CRMs.)

Before comparing individual platforms, it helps to establish what actually matters. The criteria below apply regardless of which vendor you’re considering.

AI-native integration. The distinction between bolt-on AI and AI-native architecture is the defining question of 2026. Bolt-on AI layers a chatbot or summarization feature on top of a traditional database. It operates on whatever data users manually entered, which is almost always incomplete. AI-native platforms capture, enrich, and maintain data automatically as work happens. The AI is the engine, not a feature. If you have to choose one criterion, choose this one.

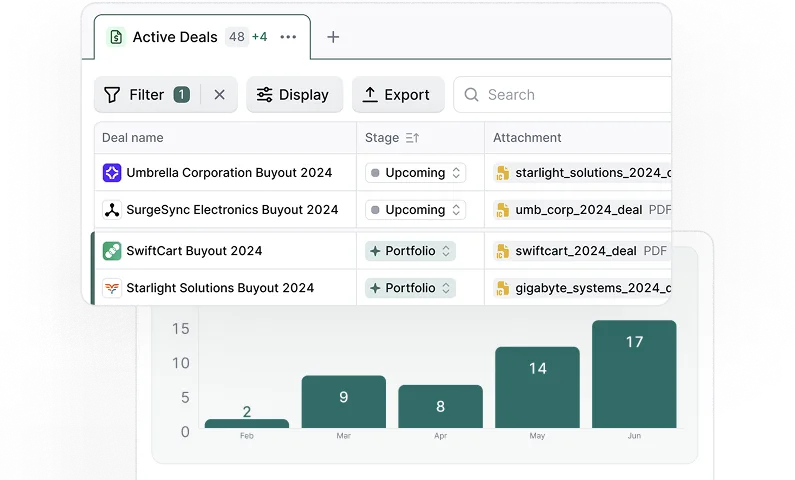

Unified lifecycle management. The platform should connect deal sourcing, due diligence, pipeline tracking, portfolio company monitoring, and LP reporting in one system. When these functions live in separate tools, the “data flywheel” (where portfolio performance insights inform sourcing and sourcing data feeds diligence) cannot spin. You end up re-entering data across systems and losing the compounding intelligence that comes from a single source of truth.

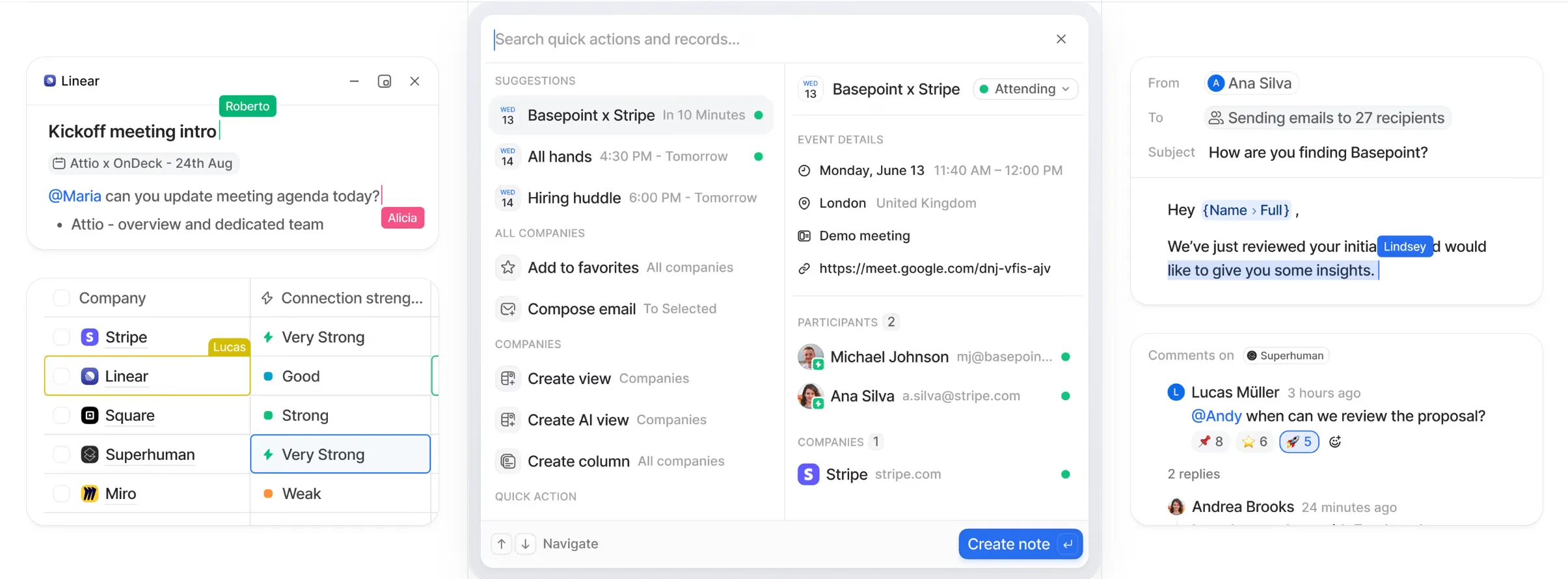

Automated relationship intelligence. This is the single most important capability separating VC CRMs from generic alternatives. The platform should auto-capture every interaction from email, calendar, and meetings, build a relationship graph, and score contact strength without manual input. If partners have to log interactions manually, adoption will collapse.

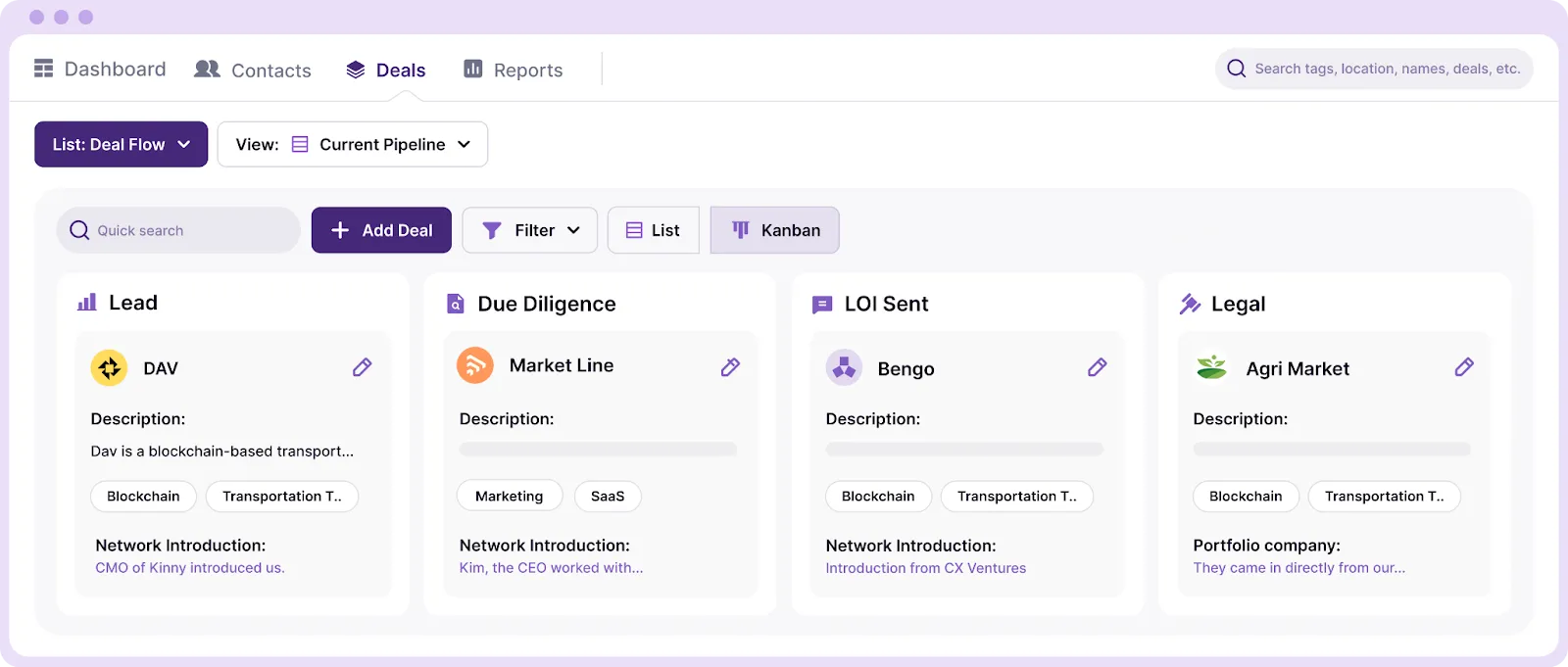

VC-specific workflows. The pipeline should reflect actual VC stages (sourcing, screening, first meeting, diligence, IC, term sheet, close, portfolio) rather than generic sales funnels. Look for thematic market mapping, founder interaction tracking, portfolio KPI dashboards, LP management, and fundraising workflows built into the product, not bolted on through integrations.

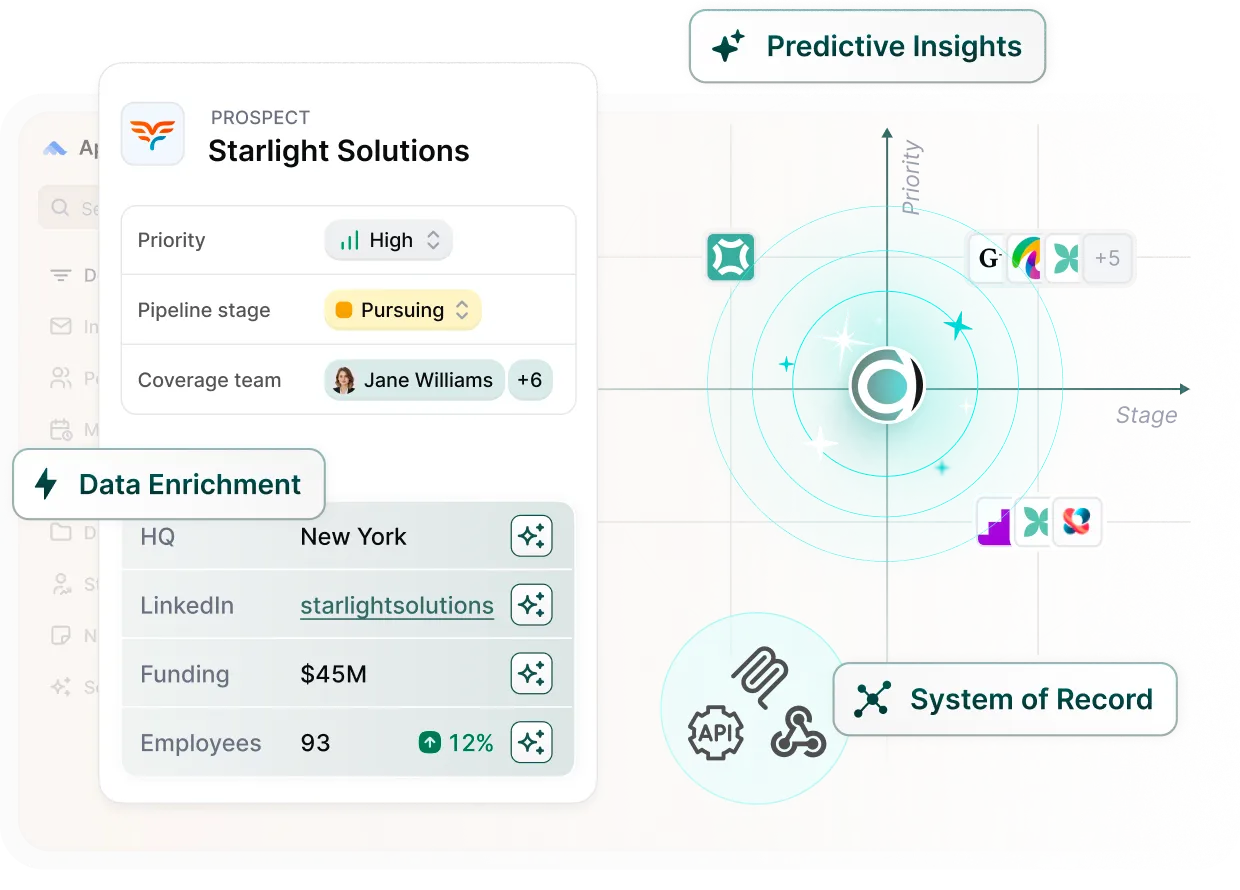

Data enrichment. Automated population from sources like PitchBook, Crunchbase, Preqin, and S&P Capital IQ covering funding history, headcount, revenue estimates, and leadership changes. Platforms that bundle enrichment data can reduce or eliminate separate data subscriptions, which is a meaningful cost advantage at scale.

Data security and compliance. Enterprise-grade security, compliance-ready infrastructure, and ethical walls for institutional investors managing multiple funds with different mandates.

We’ve organized this section by platform category rather than a ranked list, because the right choice depends heavily on your firm’s size, stage, and priorities. We start with our own platform (we’re transparent about that), then cover purpose-built competitors, generic CRMs adapted for VC, and the newest market entrant.

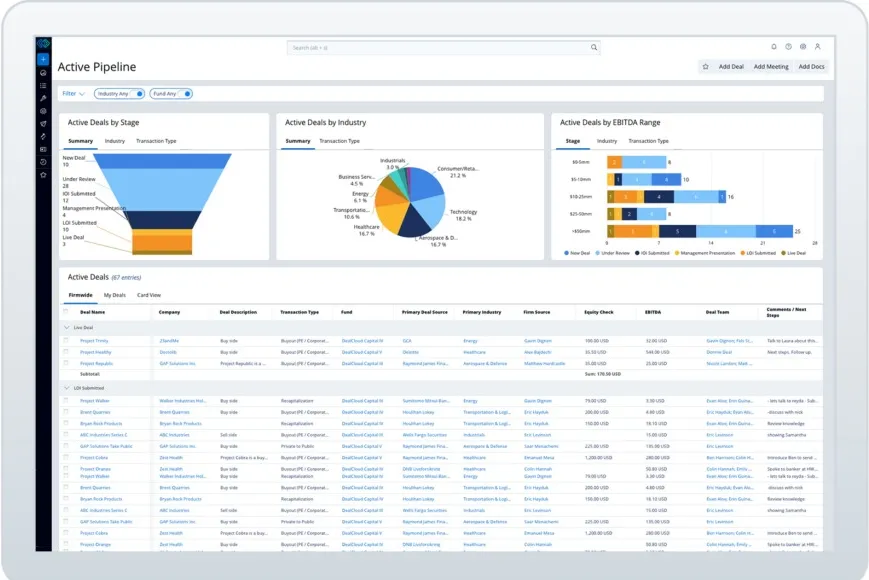

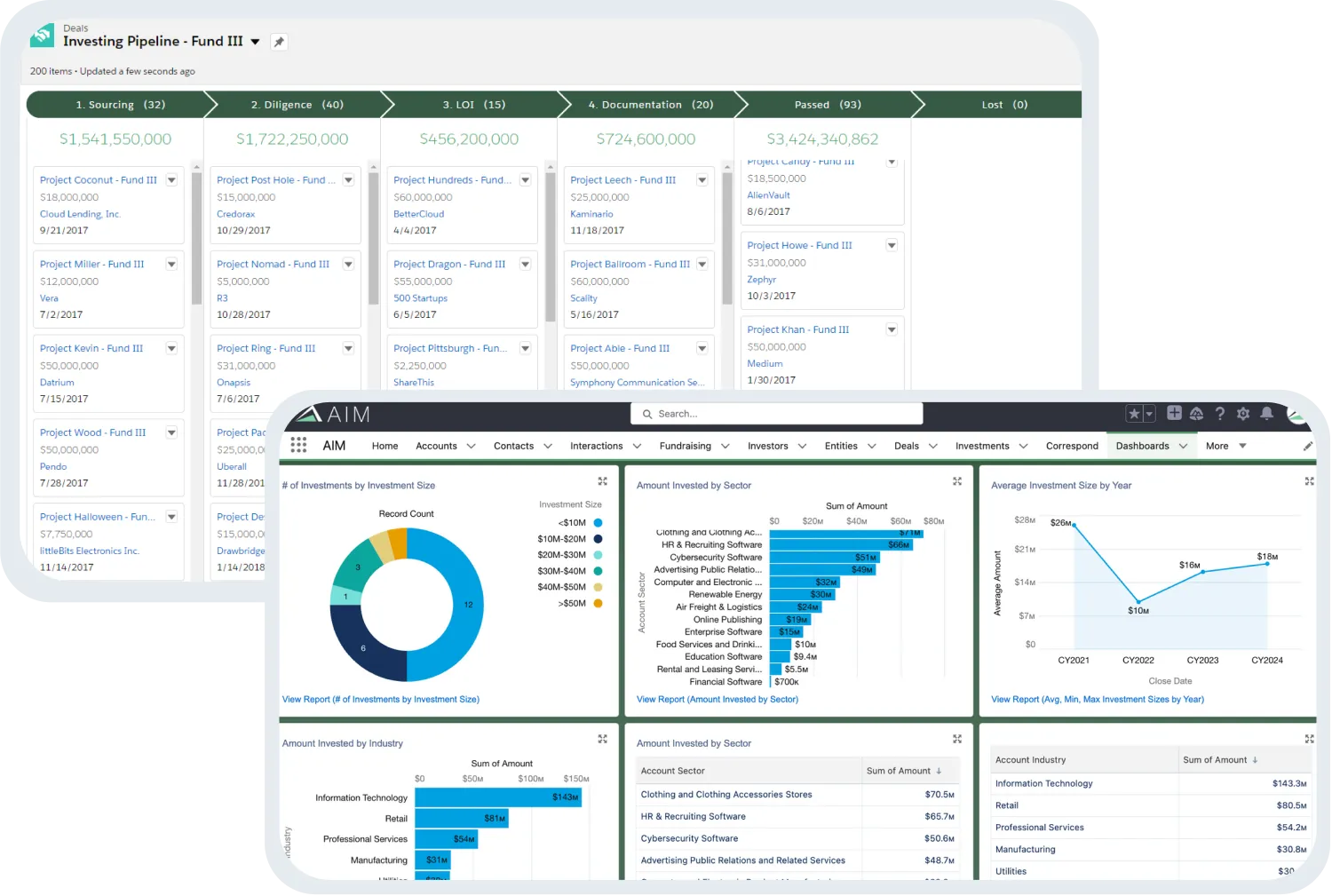

Meridian is an AI-native intelligence platform designed for private markets. We combine CRM, workflow automation, Scout AI agents, and 26 million+ company records into a unified system of record that covers the full investment lifecycle, from sourcing and diligence to IC management, portfolio tracking, and LP reporting.

The core idea is simple: eliminate manual data entry and unify proprietary data (your emails, meeting notes, and internal assessments) with public data (funding rounds, headcount changes, leadership moves) so your team sees a complete, actionable picture from a single screen.

Key capabilities. AI-powered sourcing that proactively suggests deals and maps markets based on your firm’s mandate. Automated deal and relationship tracking that captures every interaction from your inbox, building institutional memory without asking anyone to log anything. Unified portfolio intelligence that monitors company performance in the same system where deals are managed. Scout AI agents that autonomously research sectors, surface opportunities, and compile LP-ready reports.

Implementation. Implementation takes four to six weeks, compared to months for enterprise alternatives.

Trade-offs to consider. We are newer to market than legacy players like Affinity or DealCloud. Our initial product focus has been PE and institutional investors, and VC-specific features continue to expand. Firms that need a tool with a decade of VC-specific iteration may want to evaluate Affinity alongside us.

Learn more about our venture capital CRM and deal sourcing capabilities.

Affinity

Affinity is the category leader in relationship intelligence for private capital firms. Its patented relationship intelligence engine automatically captures interactions from email and calendar, builds a network graph, and scores relationship strength without manual input.

Recent product releases have been aggressive: AI Notetaker, Deal Assist, Automation Builder, and Affinity Sourcing all shipped between 2024 and 2026.

Affinity’s core strength is sourcing and relationship mapping. Its AI features have expanded substantially over the past two years. Where Meridian differs is in its approach to unified lifecycle management, bundled data enrichment, and an open architecture that lets you connect your data to any AI tool you want to use; where Affinity differs is in depth of relationship intelligence tooling and its larger installed base.

DealCloud (Intapp)

DealCloud, part of Intapp, has long been the standard for enterprise and institutional private capital. It offers deep customization, compliance-grade infrastructure, ethical walls between fund teams, and integration with Intapp’s broader suite of professional services tools.

DealCloud is the most feature-rich option in this category and a strong choice for large, multi-strategy firms with dedicated technology teams. Implementation timelines are much longer than lighter-weight alternatives, and the platform is designed for firms that need extreme configurability. Meridian takes a different approach with faster deployment (even with heavy customization) and unlimited-user pricing, but the two platforms serve somewhat different segments of the market. Meridian is increasingly the choice for firms that are getting ahead of the AI curve, and DealCloud remains the strongest legacy platform for firms that focus on more traditional approaches.

4Degrees

4Degrees was founded by former investors and offers solid relationship intelligence and network mapping. The platform focuses on helping deal teams leverage warm introductions and map networks, and it handles the core VC pipeline well. Its customer base includes firms across venture capital and private equity.

4Degrees is a strong option for small to mid-size VC firms that prioritize network-driven sourcing and want a simple implementation. The platform’s focus differs from Meridian’s in that it emphasizes relationship mapping and warm introduction paths rather than full-lifecycle deal management and AI-native data enrichment.

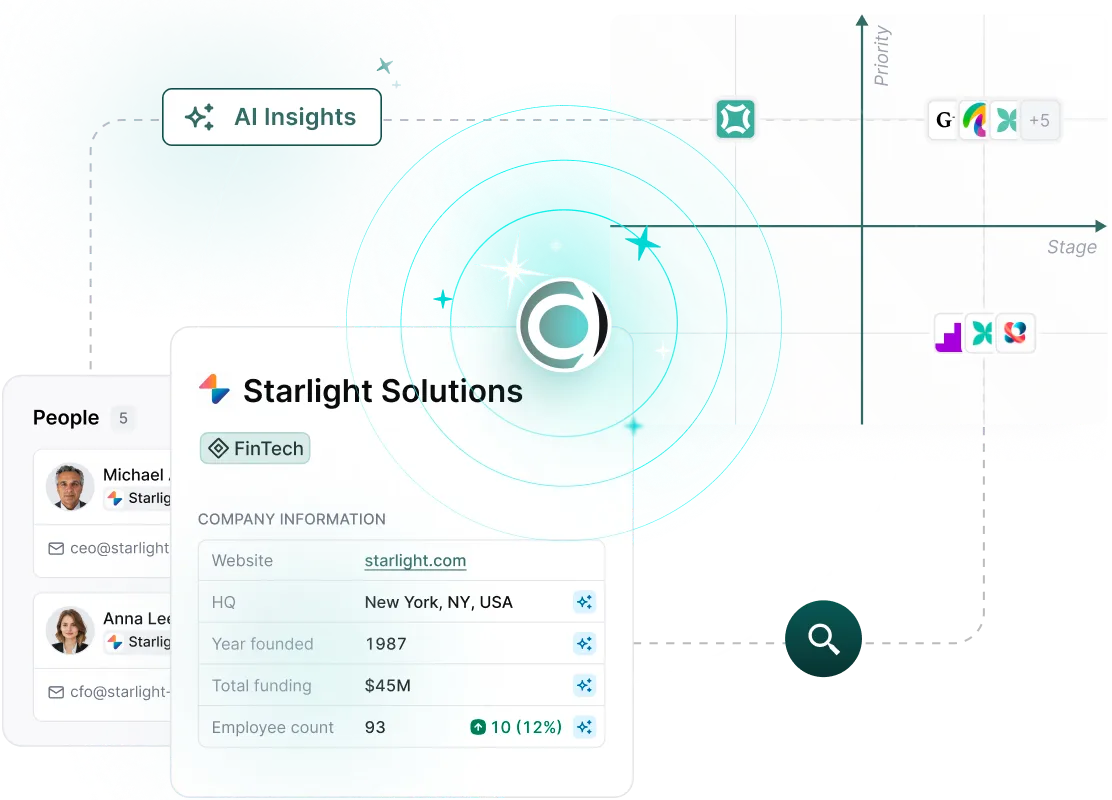

Meridian’s Scout AI agent surfaces and benchmarks new opportunities so you can find winning deals before the competition.

Attio

Attio is the fastest-growing challenger in this space. Backed by $116 million in total funding from investors including Redpoint and Balderton, it offers a Notion-like flexible data model that lets firms build custom objects and workflows without writing code. A free tier (up to three users) makes it accessible to emerging managers, and the user experience is noticeably clean. The platform resonates with tech-forward firms that value flexibility and speed.

Attio is a general-purpose CRM, not a private-markets-specific platform. Firms that need native LP management, portfolio monitoring, and VC-specific pipeline stages out of the box will need to build those workflows through configuration. For institutional firms managing multiple funds with compliance requirements, a purpose-built platform may be a better fit, but for emerging managers who want modern UX at a low entry price, Attio is compelling.

Other modern entrants include Folk CRM, Rings AI, and Clarify AI, all targeting the lightweight CRM segment with clean interfaces and lower price points. These tools work for small teams with straightforward needs.

Salesforce (with Altvia overlay)

Salesforce remains the default CRM for many institutional investors, largely because of existing enterprise agreements and IT familiarity. The Lightning Platform and AppExchange offer theoretically unlimited customization. Financial Services Cloud adds some investment management functionality.

For VC firms specifically, the calculus is harder to justify. Implementation requires dedicated admin staff and ongoing maintenance that most VC teams cannot support. Altvia has built a PE and VC layer on Salesforce since 2006, which gives firms industry-specific functionality without starting from scratch. If your firm is already deep in the Salesforce ecosystem and has the internal resources to maintain it, Altvia is a reasonable option.

For firms evaluating their CRM from scratch, the trend is moving toward purpose-built platforms. We’ve written more about this in our guide to Salesforce alternatives for private equity.

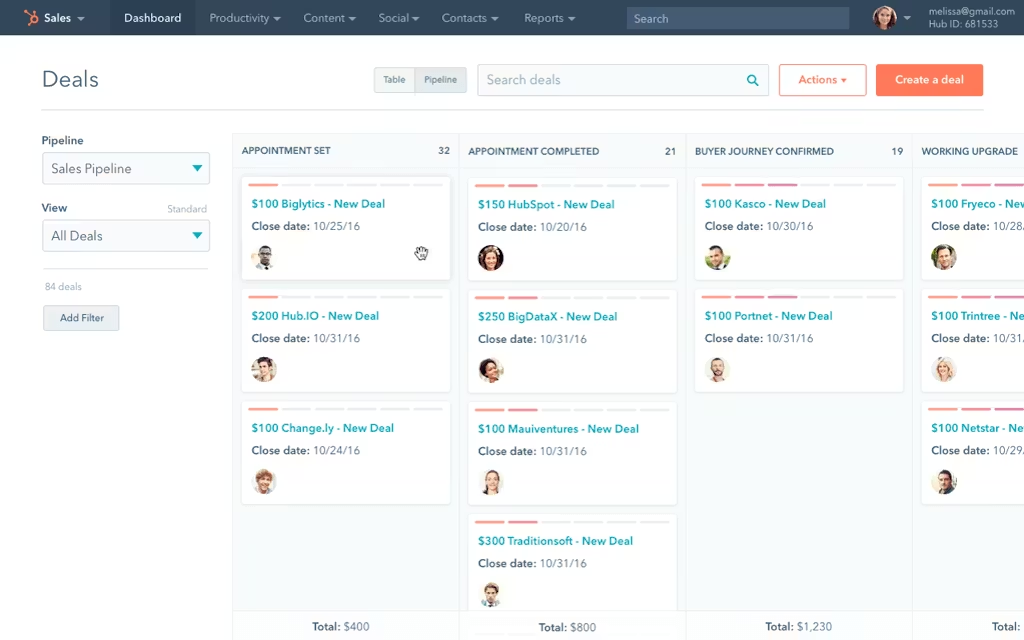

HubSpot

HubSpot offers a generous free tier and strong marketing automation, making it viable for smaller VCs on a tight budget. It works as a basic contact and deal tracker. However, it has no native VC-specific features, no relationship intelligence, and no portfolio management capabilities. For seed-stage fund managers running a lean operation, HubSpot can serve as a starting point, but most firms outgrow it as their deal flow scales.

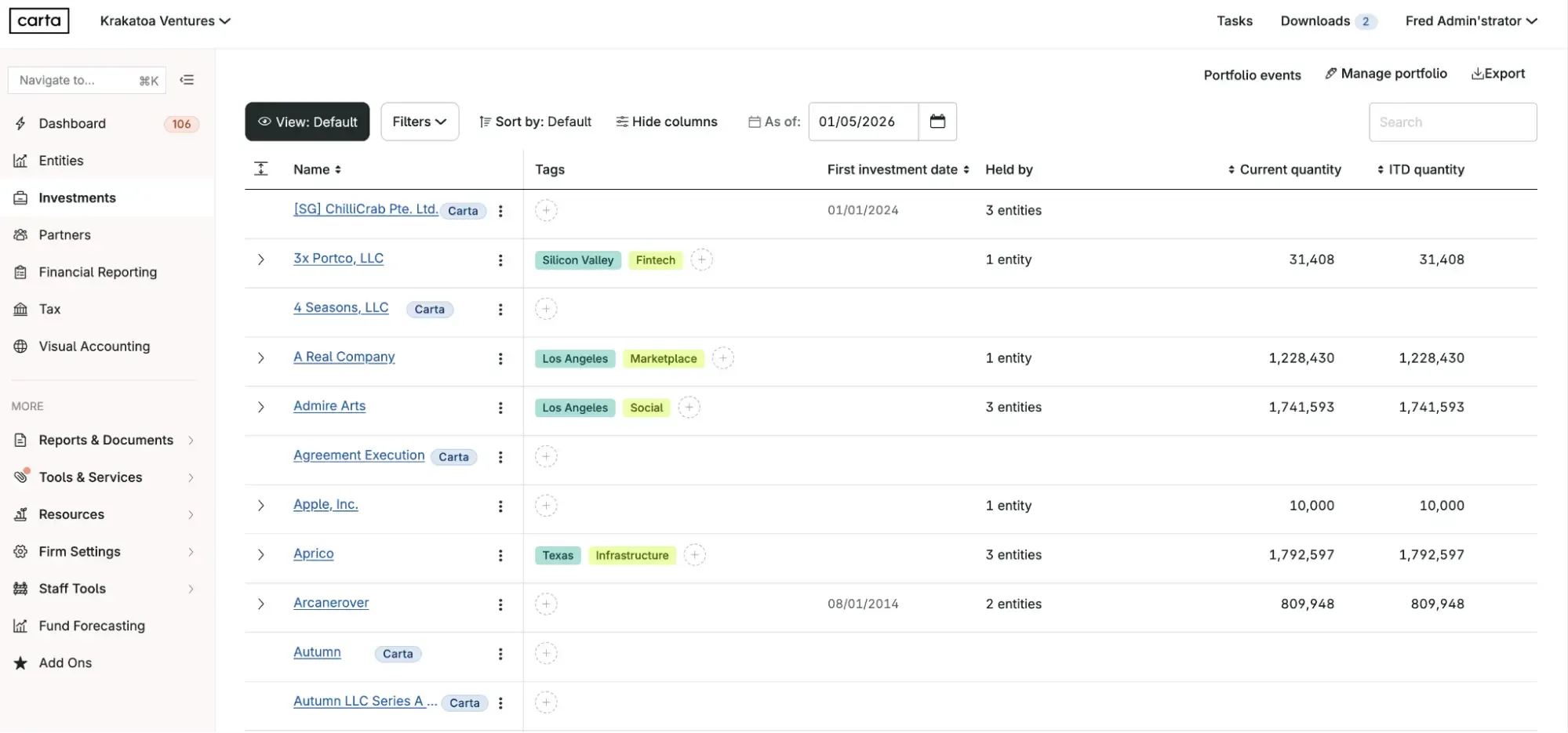

In March 2026, Carta acquired ListAlpha, an AI-powered relationship intelligence platform, and launched a CRM product for venture capital firms. Carta’s unique advantage is its existing infrastructure. It can connect CRM and deal management directly with live fund accounting data: IRR, TVPI, DPI, and carry calculations.

But the trade-offs are real. The CRM product is new and still integrating ListAlpha’s AI with Carta’s existing fund administration infrastructure. First-generation CRM products typically take time to reach feature parity with established competitors. Firms that need a battle-tested deal management system today should evaluate Carta’s CRM carefully.

The comparison table above captures features, but the more useful question is which platform fits your firm’s specific situation. Here’s how we’d think about it.

Emerging managers (Fund I–II, under $100M AUM). Budget matters, and you probably have a small team wearing multiple hats. Attio’s free tier is a strong starting point if you want a modern CRM without upfront cost. HubSpot’s free tier works for basic contact management. 4Degrees offers solid relationship intelligence at an accessible price. The risk at this stage is choosing a tool you’ll outgrow within two years, so consider platforms that can scale with you. If you’re planning to build a data-driven practice from day one, investing in an AI-native platform like Meridian pays off faster than you might expect, because the data flywheel starts compounding immediately.

Growth-stage firms ($100M–$500M AUM). You have enough deal flow that manual processes are visibly breaking, and you’re likely feeling the pain of fragmented tools. This is where the shift from generic to purpose-built CRM typically happens. Affinity, Meridian, and 4Degrees are the natural options. The deciding factors are usually whether you prioritize relationship intelligence (Affinity), unified lifecycle management with AI-native architecture (Meridian), or network-driven sourcing at an accessible price (4Degrees).

Institutional firms ($500M+ AUM, multi-strategy). Compliance, ethical walls, and multi-fund reporting become non-negotiable. DealCloud has served this tier for years with deep customization and compliance-grade infrastructure. Meridian is increasingly competing here with enterprise-grade security and private markets-native workflows. Affinity also serves large institutional clients. The key question: Do you need DealCloud’s extreme customization, or would a faster-to-deploy platform serve you better?

Firms already on Carta’s fund administration. Carta CRM deserves a serious look purely because of the fund accounting integration. If real-time IRR, TVPI, and carry data in your CRM is a priority, no other vendor matches this. Just go in with realistic expectations about a new product and have a contingency for deal management features that may still be maturing.

Firms locked into the Salesforce ecosystem. If your firm has significant Salesforce investment and enterprise IT support, Altvia’s PE/VC layer is the path of least resistance. It adds industry-specific functionality without ripping out existing infrastructure. But if your team doesn’t have dedicated IT staff managing Salesforce, the total cost of ownership (licensing plus configuration plus ongoing maintenance) almost certainly exceeds what you’d pay for a purpose-built platform.

Most VC CRM guides still frame the category around relationship intelligence and data capture. That framing is already outdated. The more consequential question is whether a platform’s AI is structural or cosmetic.

Legacy CRMs added AI as feature layers: a meeting summary tool here, a chatbot there, a predictive score bolted onto an existing pipeline view. These features operate on whatever data users manually entered, which is almost always incomplete and frequently stale. AI-native platforms take a fundamentally different approach. The AI is the engine that captures data, enriches it from external sources, maintains its accuracy over time, and acts on it proactively. The difference is not cosmetic. It determines whether the system gets smarter as your firm uses it or simply automates tasks on top of bad data.

The measurable impact is becoming clear. Industry analyses suggest that firms using AI-driven sourcing now review three to five times more qualified opportunities compared to traditional approaches. Bain & Company reported that AI-powered analysis is compressing screening timelines from days to hours. In 2021, Gartner predicted that by 2025, 75% of VC investment decisions would incorporate AI-generated insights. That prediction appears to have been broadly accurate.

The capabilities moving from experimental to essential include deal scoring against specific investment criteria, CIM auto-extraction and summarization, predictive founder success modeling, natural language querying of pipeline data, and automated market mapping. These are not future possibilities. They are shipping features in current products.

The 2026 frontier is agentic AI. Andre Retterath of Data Driven VC positioned 2025 as the transition from copilots to agents, and Bank of America projects spending on agentic AI will reach $155 billion by 2030. In the CRM context, agentic AI means systems that proactively surface opportunities matching your thesis, autonomously build sector maps, monitor portfolio companies for early warning signals, and auto-compile LP reports without being asked. We built our Scout AI agents around this premise: the system should work for you between meetings, not just respond when you click a button.

For a deeper look at how AI is changing deal workflows, see our guide to deal flow management with AI.

The competitive advantage of the next decade will not come from access to deals. Deal flow is increasingly commoditized. The advantage will come from the speed and quality of decision-making, and that depends entirely on data infrastructure.

Firms operating on a unified system of record can benchmark new opportunities against their own historical performance data. They can see which partners and contacts have been most productive sources of deals over time. They can connect portfolio performance back to the sourcing thesis that originated each investment. This creates a compounding data advantage that gets stronger with every deal, every meeting, and every quarter.

Firms running fragmented tools cannot do any of this. Their data sits in silos. Their institutional memory resets every time a team member leaves. Their LP reporting is a quarterly scramble rather than an automated output.

Consider what a unified system makes possible in practice. A partner meets a founder at a conference. The interaction is automatically logged, the founder’s company is enriched with funding history, headcount data, and revenue estimates, and the deal appears in the pipeline, scored against the firm’s mandate. When the team discusses the opportunity at the next IC meeting, the system has already pulled comparable companies from the portfolio, flagged relevant co-investors in the firm’s network, and prepared a preliminary market map. The partner’s 30-second interaction at a conference becomes a structured, data-rich starting point for diligence, without anyone entering a single field manually.

Now multiply that across hundreds of interactions per week, across every partner and associate at the firm, over years. The data compounds. The relationship graph deepens. The AI gets better at predicting which opportunities match the firm’s thesis. That is the flywheel. It only works when everything lives in one system.

The market is consolidating in this direction. Carta’s CRM launch signals that even fund administration providers see the value in connecting front-office deal management with back-office operations. The firms that adopt unified, AI-native platforms first will build data advantages that compound over time and become increasingly difficult for competitors to replicate.

For more on this shift, see our analysis of how the best firms are rethinking deal flow management.

The choice of CRM is no longer an operational afterthought. It is a strategic decision that shapes how your firm sources, evaluates, and monitors investments. Specialized tools can address isolated pain points, but only a unified, AI-native platform can provide the intelligence layer required to compete at the highest level in 2026 and beyond.

If your firm is still running on spreadsheets, a generic CRM, or a patchwork of point solutions, the gap between you and firms with modern infrastructure is widening every quarter.

See How Meridian Powers Leading Venture Capital Firms. Book a Demo.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Find out how leading PE firms are using Meridian to enhance their deal workflows.

.webp)

It depends on your firm’s size and priorities. Meridian is purpose-built for the full investment lifecycle, Affinity leads in relationship intelligence, DealCloud serves large institutions, and Attio works well for emerging managers who want a modern UX.

Venture capital requires many-to-many relationship mapping, automated data enrichment from investment-specific sources, and VC pipeline stages. Generic CRMs need months of configuration and ongoing admin to approximate these features, and most VC teams lack the resources to maintain them.

AI-native means the AI captures, enriches, and maintains data automatically as your team works. Bolt-on AI runs on whatever users manually entered, which is usually incomplete. The practical difference: AI-native platforms get smarter over time while bolt-on AI automates tasks on top of stale data.

Six criteria matter most: AI-native integration, unified lifecycle management, automated relationship intelligence, VC-specific workflows, automated data enrichment, and enterprise-grade security.

The most effective approach combines automated intake into the pipeline, AI-powered screening against your investment criteria, and relationship context that flags warm introductions from high-value contacts. The goal is reducing time on unqualified deals so partners focus on opportunities that fit the mandate.

Table of Contents

Making the internal case to your firm is the real bottleneck for AI adoption. Here's how to make the strongest case, step by step.