Meridian MCP is live! Connect your deal sourcing data directly to Claude

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

AI-powered deal software, CRM fatigue, and what 40+ firm conversations reveal about the tech stack actually winning in private markets right now.

There's a conversation I have almost every week. It goes something like this:

A principal at a mid-market PE firm tells me they're evaluating new deal management software. I ask what they're currently using. They pause, then start listing: DealCloud for the pipeline, PitchBook for company data, Carta for cap table management, Notion for diligence tracking, Claude for memo drafting, Slack for everything else, and three or four more tools that "kind of overlap but we haven't consolidated yet."

Then they say the thing I always wait for: "It's a lot."

That's the state of software in private markets right now. Not chaos, exactly. But close.

The private equity and venture capital tech stack problem didn't happen overnight. It's the product of a decade of point-solution proliferation, where every workflow pain spawned a new vendor, and every new vendor required an integration that required a Zapier workflow that required someone to maintain it.

The 2015 to 2022 era was good for SaaS companies selling into investment firms. Data providers, CRM vendors, portfolio monitoring tools, fundraising platforms, LP reporting tools, ESG trackers — all of them carved out a seat at the table. Firms bought them, often without a coherent strategy, because the individual ROI argument for each tool was easy to make. Of course you need a better way to track deal flow. Of course you need automated LP reporting. Of course you need real-time portfolio data.

What nobody was asking was: How do all these tools talk to each other? And who owns that question?

The answer, at most firms, was nobody.

Here's what tool fragmentation actually costs investment teams. And it's not just the SaaS spend…

Context switching is expensive.

Research from Gloria Mark at UC Irvine found that after an interruption, it takes an average of 23 minutes and 15 seconds to fully regain deep focus on a task. For an investment professional whose edge is judgment and synthesis, that's not a rounding error. That's hours per week spent recovering from context switches that should never have happened.

Institutional knowledge lives in the wrong places.

At most firms, the real story of a deal lives in Slack threads, personal Notion pages, and email chains that are functionally invisible to anyone who wasn't in the room. Why you passed, what the founder said in that first call, what the comp set looked like when you first saw them: That’s all critical context, but when a senior partner leaves, that knowledge leaves with them. The CRM is full of structured fields that nobody filled out correctly.

Integration debt compounds.

Every point-to-point integration you build is a liability, not an asset. APIs change. Vendors get acquired. That Zapier workflow your ops associate built in 2022 breaks silently, and nobody notices for three weeks. The more connections you have between tools, the more surface area for failure.

Onboarding gets worse every year.

When a new associate joins and has to learn eight different tools before they can do their job, you're paying a productivity tax and a morale tax. The firms growing fastest right now are the ones where new hires are productive in weeks, not months.

After talking to 40+ investment firms across conversations, demos, and market research calls, from emerging managers up through mega-cap shops, I’ve spotted a few clear patterns on the technology side.

DealCloud built a dominant position in the mid-market over the past decade. It's deeply embedded, well-understood, and has a solid feature set. It's also showing its age.

The complaints I hear most often: implementation timelines are measured in months (sometimes quarters), customization requires professional services for anything non-standard, and the UX feels built for compliance officers rather than deal professionals. For firms that live and die by velocity, a 6-month onboarding is a competitive disadvantage, full stop.

The firms evaluating alternatives in 2026 aren't necessarily unhappy with their CRM's feature set. They're unhappy with the implementation experience, the cost of change, and the feeling that their software can't keep pace with how they actually work. Affinity captured some of this dissatisfaction early by leading with relationship intelligence. Newer entrants are betting on faster implementation, better AI integration, and pricing models that make more sense for emerging managers.

While that's the bet we're making at Meridian, we’re also betting on something more important for private markets investing firms: We built the platform specifically for the way PE, VC, and IB teams actually work. And we measure ourselves on how fast firms are fully operational, not just contracted.

If your firm doesn't have a position on how your deal team uses AI, you're already behind. This isn't speculative anymore. It's observable in the market. G2 reports that 57% of companies already have enterprise AI agents running in production, and another 22% are in the pilot stage.

The investment professionals who integrated AI tools into their workflow early (specifically for deal analysis, memo drafting, company research synthesis, and meeting prep) are operating at a materially different pace than those who haven't. Across the firms we work with, deal teams consistently report saving multiple hours per deal on research and documentation tasks alone. Across a 100-deal-a-year pipeline, that compounds significantly.

Claude has become the dominant choice for sensitive deal work, primarily because of how firms think about data privacy and confidentiality. ChatGPT is used broadly for general tasks, but has lost trust in the deal room for anything involving proprietary information. The pattern that's winning is AI as a layer on top of your existing data, not a replacement for human judgment.

The firms struggling with AI adoption tend to share one characteristic: They're trying to bolt AI onto broken workflows instead of redesigning the workflow around what AI makes possible.

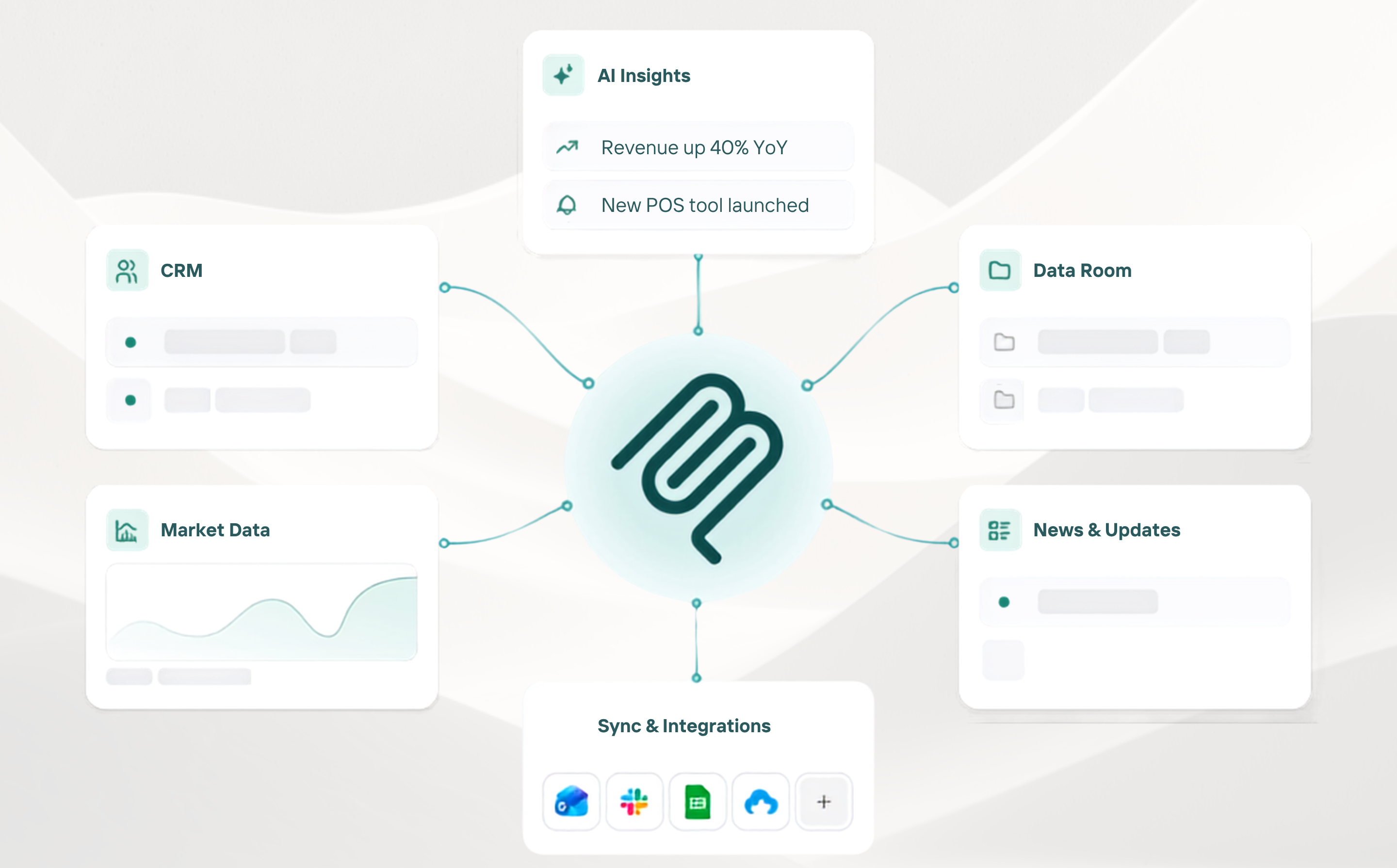

The best sourcing data in the world is worthless if your IR team can't access it. The most detailed portfolio company notes mean nothing if they live in a folder that nobody knows exists.

The firms building real competitive advantage right now aren't necessarily buying more data. They're getting serious about connecting the data they already have. Sourcing intelligence should inform investment decisions. Portfolio company performance should surface patterns for the next fund's thesis. Historical deal data should make underwriting faster.

This sounds obvious. In practice, it requires genuine commitment to data hygiene and system design that most investment teams haven't prioritized. The operational infrastructure is unsexy work. It's also increasingly the differentiator.

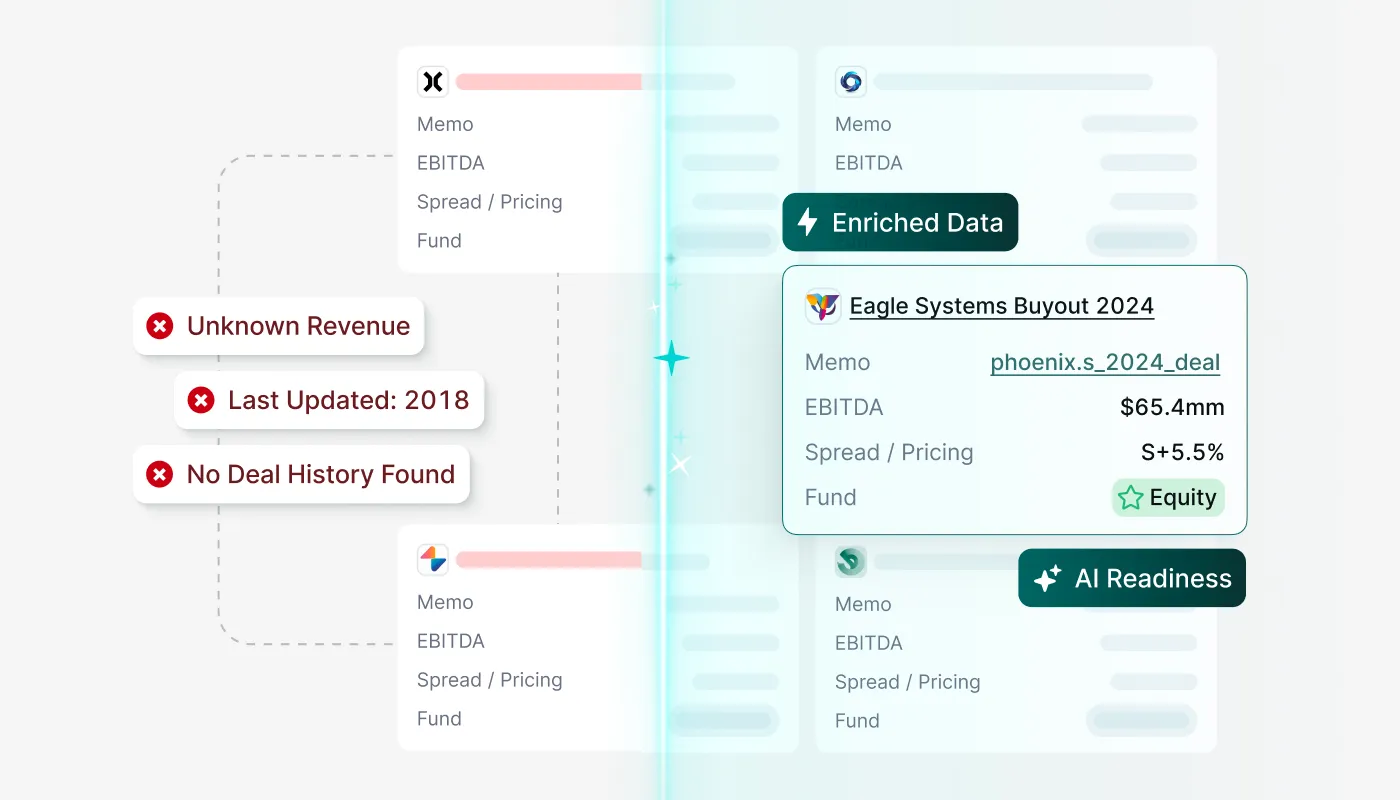

PitchBook has been the default for private company data for years. That position is under real pressure. Grata's rollup strategy is creating a credible challenger with differentiated coverage in the lower middle market. AI-driven enrichment tools are letting firms build custom data pipelines that supplement or replace parts of their existing subscriptions.

The PitchBook bundle made sense when the alternatives were worse. As the alternatives catch up, expect more firms to disaggregate their data stack rather than keep paying for coverage they don't use.

The investment teams I see executing well on the technology side don't share a specific vendor list; they share a philosophy.

For all the tools selling into private markets right now, there are still genuine gaps.

Relationship intelligence at the fund level.

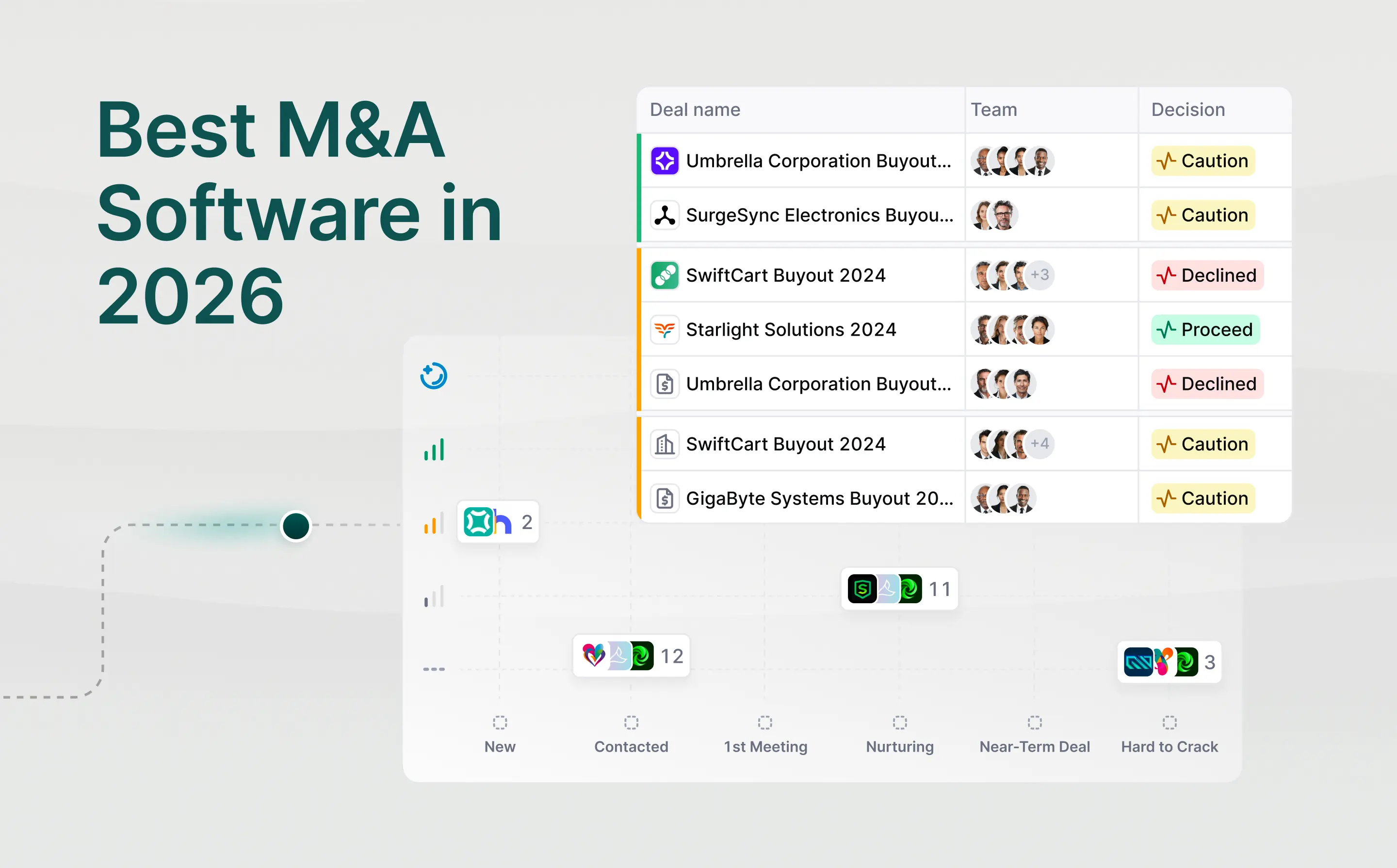

Most CRMs track deals and contacts. Very few do a good job of surfacing relationship context across an entire firm's network. Who knows who, how warm a connection is, what the history looks like across multiple touchpoints — these things matter enormously in a relationship-driven business.

Portfolio company data integration.

For many firms, getting portfolio company financial data, operating metrics, and board materials into a single view that doesn't require a team of analysts to compile every quarter is still harder than it should be.

Institutional memory.

The problem of capturing and surfacing tacit knowledge, why you passed on a deal, what you learned in diligence, and what a founder said that changed your view, remains largely unsolved. Some firms are experimenting with AI-assisted note capture and synthesis. Most haven't cracked it.

Workflow-native AI.

The pattern right now is mostly "export to Claude, get output, paste back in." What's coming, and what will separate the next generation of deal software from the current one, is AI that lives inside the workflow rather than alongside it.

Before evaluating any new software, do this:

Most firms will find two or three tools that survive that question easily. They'll find a few more that survive it reluctantly. And they'll find a handful that only exist because canceling them requires a conversation nobody's had yet.

The goal isn't the fewest tools. The goal is the most coherent set of tools for how your team actually works. Context as king. Data that flows. Workflows that don't require six apps to complete one task.

The firms that get there first will have a real operational advantage. Not just in efficiency, but in the quality of decisions, the speed of execution, and the institutional knowledge that sticks around when people leave.

The stack is infrastructure. And in private markets, infrastructure is strategy.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Table of Contents

The top investment banking CRM and deal management platforms for 2026, compared on automated capture, mandate management, and time to adoption.