Meridian MCP is live! Connect your deal sourcing data directly to Claude

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

PE is built around the ownership timeline. IB is built around relationships, mandates, and live processes. Get the wrong unit of work in your CRM, and reporting, attribution, and pipeline visibility all break.

From the outside, both private equity and investment banking involve deals, investor relationships, and financial data. But from the inside, the operational reality, and the systems required to support it, are very different.

Private equity (PE) is built around fund lifecycles, capital deployment, and long-term ownership oversight. Investment banking (IB) is built around relationship cultivation, mandate origination, and process execution.

These differences show up most clearly in three places:

This article breaks down how PE and IB firms operate, where their tracking and reporting requirements diverge, and why that divergence makes the case for purpose-built CRM architecture.

Differences in operating models have direct implications for the systems both investment banks and PE firms use to manage their work.

Investment banking workflows are built around transactions. The goal is to strengthen client relationships, execute deals, and move on to the next opportunity. And everything flows from that model, from client coverage lists and pitch activity to deal pipelines and buyer outreach during a live process.

When a transaction closes, the engagement ends. The CRM follows that same logic: track the relationship over an extended period of time, manage the pipeline, and log the activity.

Private equity operates on an entirely different timeline. Rather than working towards a sale, you’re working towards a purchase. Firms must raise capital from LPs, deploy that capital into portfolio companies, actively manage those investments, and report performance back to investors, often over a fund cycle spanning a decade or more.

Each of those phases generates its own layer of records: fund structures, LP commitments, capital call schedules, and portfolio performance metrics. All of which need to be tracked, updated, and reported on continuously.

Private equity firms need to be able to maintain a continuous, living set of data across the entire fund lifecycle. From the first LP conversation to a fund’s final distribution, every phase adds information the firm cannot afford to lose track of.

This includes LP relationships and capital commitments, potential deals, live opportunities, and portfolio companies.

LP relationship management goes well beyond contact tracking. Private equity firms need to maintain a full history of each investor's commitments across capital commitments, their distribution activity, communication cadences, and any reporting obligations that apply specifically to them.

These relationships span decades, and records have to be able to support these timelines.

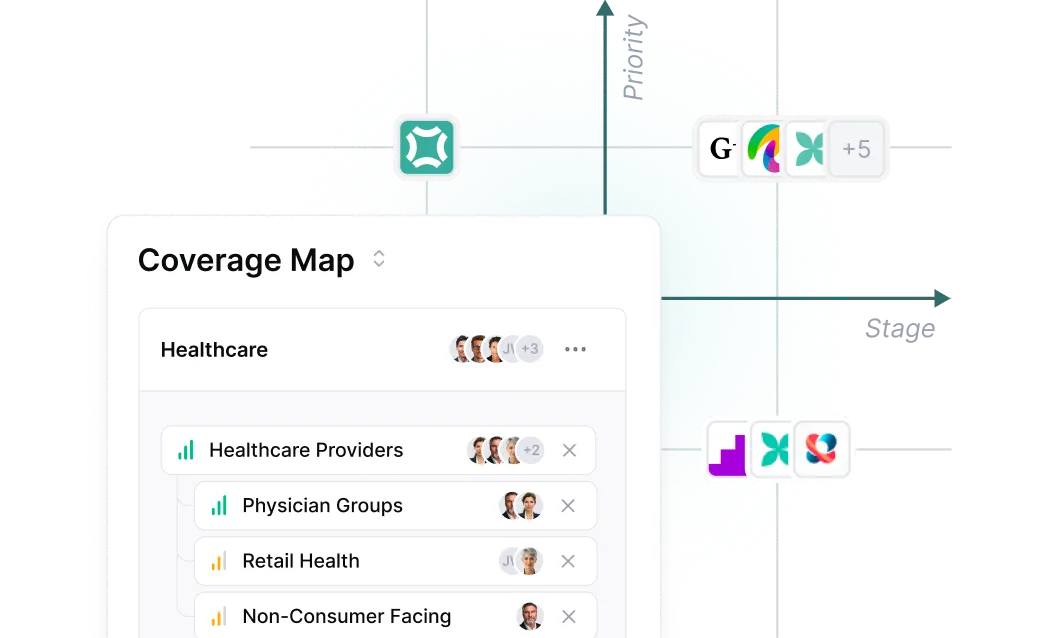

Before capital is deployed, firms are running a continuous sourcing operation. That means tracking deal flow, intermediary relationships, sector theses, and early-stage company conversations that may not convert for months or years.

PE sourcing records must accommodate the fact that a company logged today may not be ready to sell for years.

Once a deal moves into active consideration, the tracking requirements deepen. You need to log IOIs, management meetings, diligence workstreams, and deal team activity. Then, this all has to be tied to a single opportunity record that captures how conviction developed over time.

That record becomes the foundation for portfolio monitoring and eventual exit tracking.

Post-close, you have to monitor operational KPIs, valuation marks, board and operating cadence, value-creation workstreams, and management team performance across every portfolio company simultaneously.

That information feeds LP reporting and fund-level performance calculations. It needs to be well-structured and can’t be scattered across spreadsheets and email threads.

Meridian was built by and for PE professionals, providing tools that keep your firm strategic, efficient, and ahead of the game.

Investment banking is a relationship-to-revenue business, and the gap between the two can span years. Bankers invest significant time nurturing relationships long before any mandate materializes. Without a clear way to distinguish high-potential relationships from low-probability ones, time and resources are easily misallocated.

That makes relationship tracking strategically critical. And once a mandate is won, the operating model shifts to execution.

In IB, the client relationship record is the center of gravity for everything else. Bankers track coverage ownership, interaction history, meeting cadence, and relationship strength.

Critically, you also need to be able to track fit signals to prioritize where they’re spending their time. A well-maintained client record serves as an assessment of when and how a relationship is likely to generate revenue.

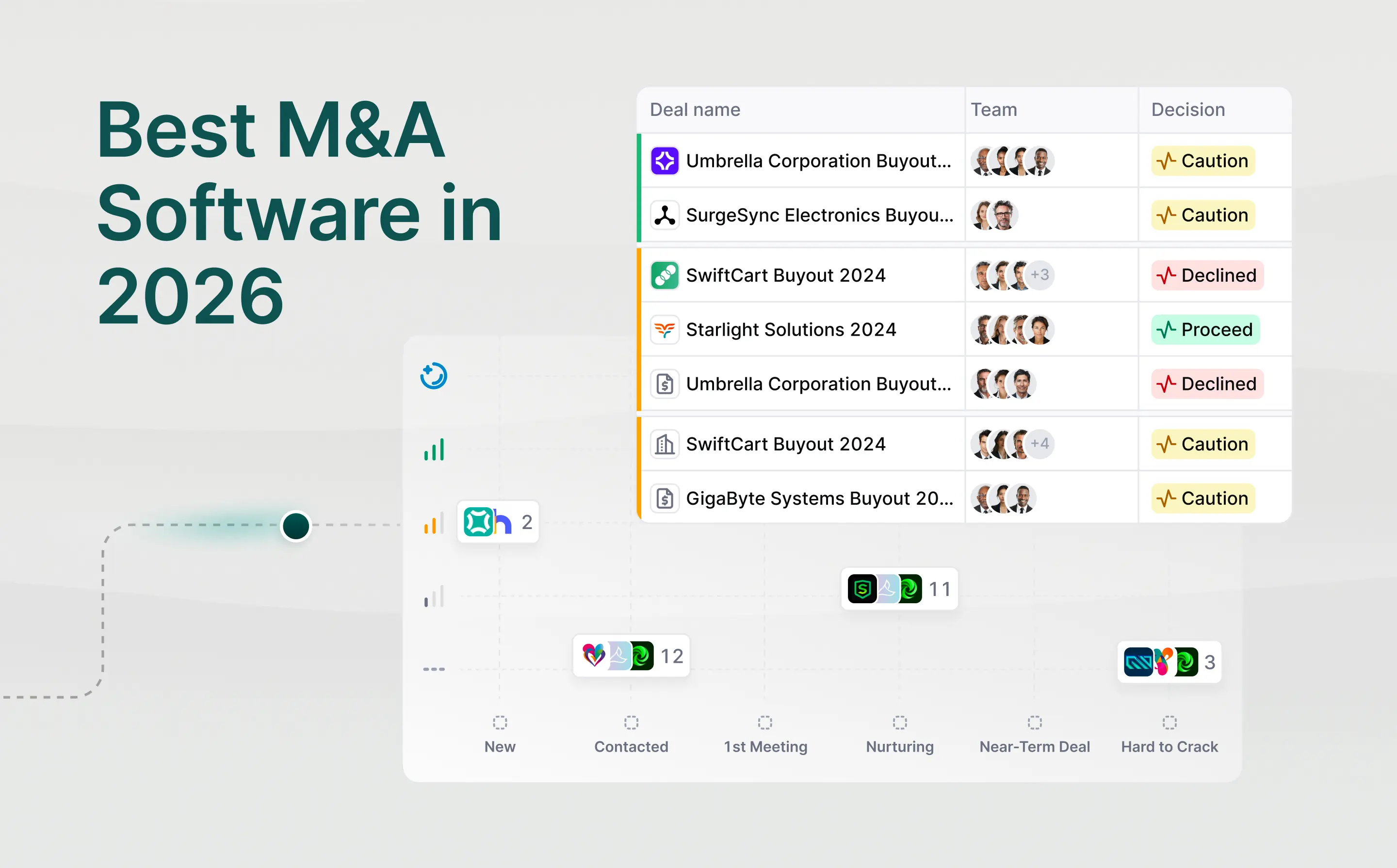

During an active process, banks manage buyer lists, process milestones, NDA tracking, management presentation schedules, and bid timelines. The system needs to support deal execution at pace, with clear visibility into where each process stands.

When the deal closes, that activity record feeds back into the credential and relationship layers, ready to support the next cycle.

Pitch activity is where relationship capital gets converted. Advisors track which clients were pitched, which materials were used, what the outcome was, and why they won or lost.

Over time, that data informs how you refine your sector positioning, improve your pitch strategy, and prioritize future interactions. A strong pitch tracking record helps you avoid repeating losing approaches and double down on what works.

When a relationship converts, it becomes a mandate, and the tracking shifts to engagement management. This means logging fee structures, deal economics, engagement terms, and key milestones.

After close, the transaction becomes a credential that signals sector expertise, transaction type experience, and relationship depth to future clients. That credential library is a core competitive asset that’s continuously updated and referenced in pitch development.

When CRMs fail in private markets, it’s often for a simple reason: they model the wrong unit of work.

In investment banking, you’re looking at relationships and mandates. Once a deal goes live, the pressure shifts to process execution. But relationship context still matters, because future mandates depend on it.

In private equity, the unit of work is the fund lifecycle and ownership timeline. Deals span years, not months, and every interaction, decision, and data point needs to persist across that timeline.

That difference shapes everything a CRM needs to do.

For example, imagine a partner at a PE firm gets an email from an LP: “Can you walk me through our unfunded commitment and recent distributions across Fund III?”

To answer, they need a full view across capital calls, distributions, historical allocations, and LP communications. That information is rarely tied to a single “deal.” It lives across the fund, across time, and across multiple systems if the CRM isn’t built properly.

Now compare that to an IB VP preparing a client update: “Where do we stand on buyer outreach and IOIs?”

They need a clean view of outreach status, which buyers have engaged, who has signed NDAs, and which indications of interest have come in. The CRM needs to reflect real-time deal progression, while at the same time preserving valuable context around other relationships that will enable the VP to close future business.

Both workflows require systems that are uniquely tailored to their needs.

A PE CRM needs to behave like a system of record for the entire investment lifecycle, not just a deal tracker.

That means capturing and connecting:

The key requirement is continuity. A company reviewed two years ago should reappear with full context intact. And an LP conversation should tie back to fund performance and reporting without manual stitching.

That means you need a system that structures data around funds, investments, and relationships, with data enrichment layered in, so teams don’t have to rebuild context from scratch every time.

Without that, private equity firms fall back on spreadsheets, inboxes, and individual memory, and that’s where workflows break.

An IB CRM needs to support both live deal execution and long-term advisory relationship management.

While banking workflows are often tied to active mandates, the work isn’t purely transactional.

Bankers spend years building trust with founders, executives, sponsors, and corporate development teams before a mandate is ever signed. That’s why it is called advisory. And success depends as much on the relationships behind the deal as the deal process itself.

Your CRM has to support that broader relationship arc while also helping teams run a tight process once a deal goes live.

Core requirements include:

The balance matters. A banker always needs to know where a deal sits at any point in time, as well as the state of any given relationship and how that shapes next steps and conversations.

That means an IB CRM needs to preserve advisory context, not just process data. It should show who knows the client, what has been discussed, where the opportunity originated, and how that relationship has developed across multiple pitches, mandates, and outcomes.

Trying to retrofit a generic CRM to PE or IB workflows means accepting permanent workarounds, data gaps, and reporting that never quite ties out.

PE firms need a system that can hold LP relationships, fund structures, capital activity, and portfolio performance in a single reconcilable data model. Investment bankers need one built around relationship prioritization, pitch activity, mandate execution, and credential reuse.

Meridian is purpose-built for both.

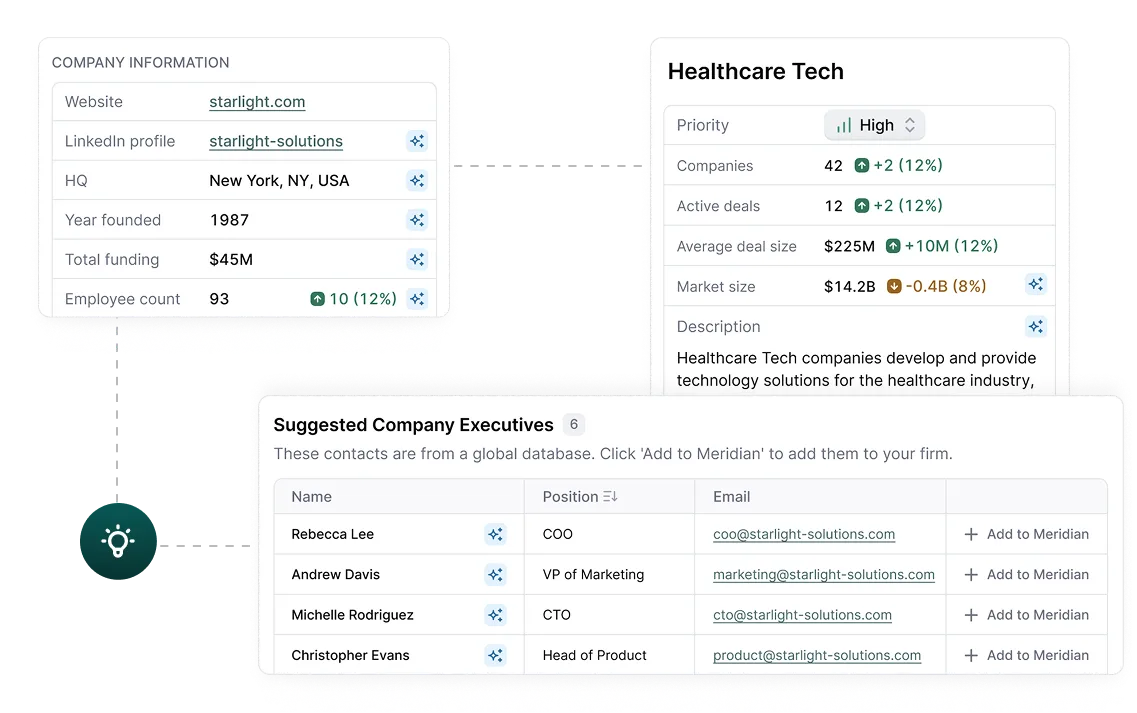

For PE firms, it functions as an AI-native sourcing and relationship intelligence platform. The tool can:

For bankers, it supports the full sell-side execution cycle:

Underpinning the tool is Scout AI, which handles data extraction from unstructured documents and continuously enriches company profiles.

So whether you're a PE investor tracking potential deals over multi-year cycles or a banker managing a live process, you're working from a single trusted database.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Table of Contents

Compare purpose-built M&A deal management platforms for 2026 and find the right fit for your corporate development team.