Meridian MCP is live! Connect your deal sourcing data directly to Claude

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

PE and VC look similar on paper. The sourcing mechanics, fundraising workflows, and reporting obligations are not. Here's where the operating models actually diverge — and what it costs when your CRM doesn't reflect that.

Both private equity and venture capital firms raise funds from LPs, deploy it into companies, and work to return it at a multiple. The surface-level similarities are real, but they mask operating models that differ in really meaningful ways.

But key differences between private equity and venture capital lie in how each type of firm sources deals, runs a fundraise, manages the mechanics of closes, and approaches reporting. This has direct implications for how firms build their teams, structure their workflows, and choose the infrastructure that supports them.

This article breaks down where PE and VC differ and what it means for the tech stack each firm needs to operate effectively.

Private equity and venture capital are both relationship businesses. And from the outside, the operational overlap looks significant. But the relationship network each type of firm has to maintain, and the workflows that sit on top of it, are structurally different.

PE relationships are built around intermediaries, management teams, and a concentrated LP base with long-duration commitments. Venture capital firms maintain a much wider network; it spans founders at the earliest stages of company building, scouts, accelerators, and co-investors, alongside a diverse LP base.

Those differences shape how each firm sources deals, how it manages fundraising, and what its operational infrastructure needs to support.

Deal sourcing is the foundation of both PE and VC, but the day-to-day couldn’t look more different.

In private equity, sourcing runs on two parallel tracks.

Both approaches require comprehensive relationship management. Which banks send the best deal flow in your sectors? Who found the last three deals that made it to IC? That attribution data is operationally valuable and needs to be tracked deliberately.

In venture capital, the funnel looks different from the first touch.

Most early-stage deals enter through warm introductions from founders, co-investors, former colleagues, or scouts embedded in startup communities. Accelerator demo days, university networks, and online communities add volume to the top of the pipeline.

Proactive, outbound deal discovery and network-driven sourcing are also big in venture capital. Firms actively look for promising start-ups by tracking early signals, monitoring databases, and reaching out to founders before they start to raise funds.

And referrals are a compounding sourcing channel that private equity firms rarely rely on in the same way. Every founder who gets backed has a whole network of other potential opportunities.

Progress in the funnel is measured by conviction: Has this company cleared the bar on founder quality, market size, and timing?

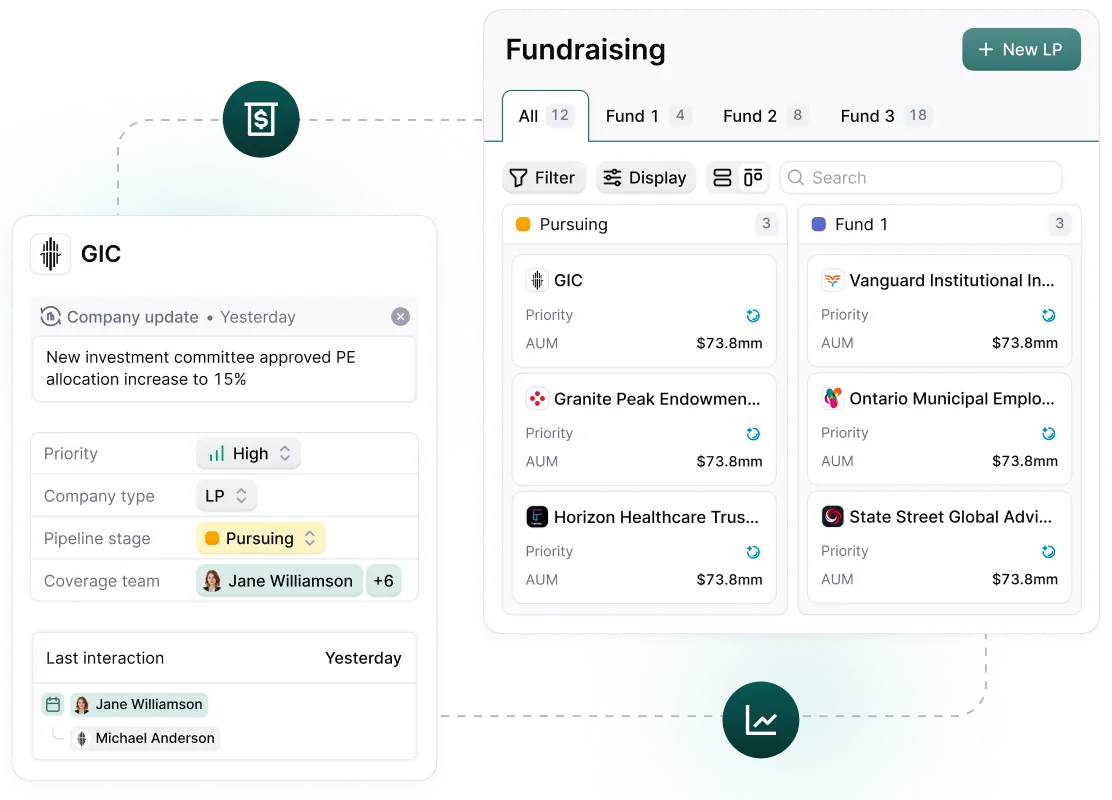

Both PE and VC firms raise from limited partners. But the operational reality of running a fundraise generates different workflow demands, different data hygiene requirements, and different consequences when records aren't maintained properly.

In private equity, the LP base is typically institutional, ranging from pension funds and endowments to sovereign wealth funds and family offices writing large checks.

As a result, there are fewer of them, which means each relationship carries more weight and requires more deliberate management. And a missed follow-up can cost a commitment.

The mechanics between first and final close also create operational overhead.

LPs who come in at first close are entitled to returns that reflect their earlier commitment, while LPs who join later go through an equalization process: paying into the fund at a standardized rate so that all investors are on equal footing at final close.

All of this puts pressure on investor relations. Managing IR cleanly requires precise records of commitment dates, capital call schedules, and distribution waterfalls. If your LP data lives across spreadsheets and email threads, equalization becomes an issue of data integrity.

Ongoing reporting adds another layer. Institutional LPs may have their own reporting templates and compliance requirements, which makes the data you track during the fund's life a contractually obligated output.

In venture capital, the LP base is often broader and more diverse. A VC fund might have dozens of LPs, like high-net-worth individuals, family offices, and increasingly, non-traditional investors (think founders and operators who bring strategic value alongside capital).

That diversity creates its own operational demand. Managing relationships with varying check sizes, communication preferences, and reporting expectations requires a different kind of operational discipline.

The fundraise structure adds another layer. Rolling closes are more common in VC, which means the fundraise itself can span a year or more. New LPs are onboarding while the fund is already deploying capital, which compounds the data management challenge.

Who has signed? Who has funded? Without a clean system of record, those questions don't have reliable answers, and your fundraising operations suffer.

The deeper issue in both models is the same: Fundraising creates a data foundation that the rest of the fund's operations run on. LP records established during a fundraise inform capital calls, distributions, reporting, and re-up conversations for the next fund. And getting that foundation right is a compounding operational advantage.

Meridian is your team’s ultimate context provider, driving better deals while minimizing manual data entry.

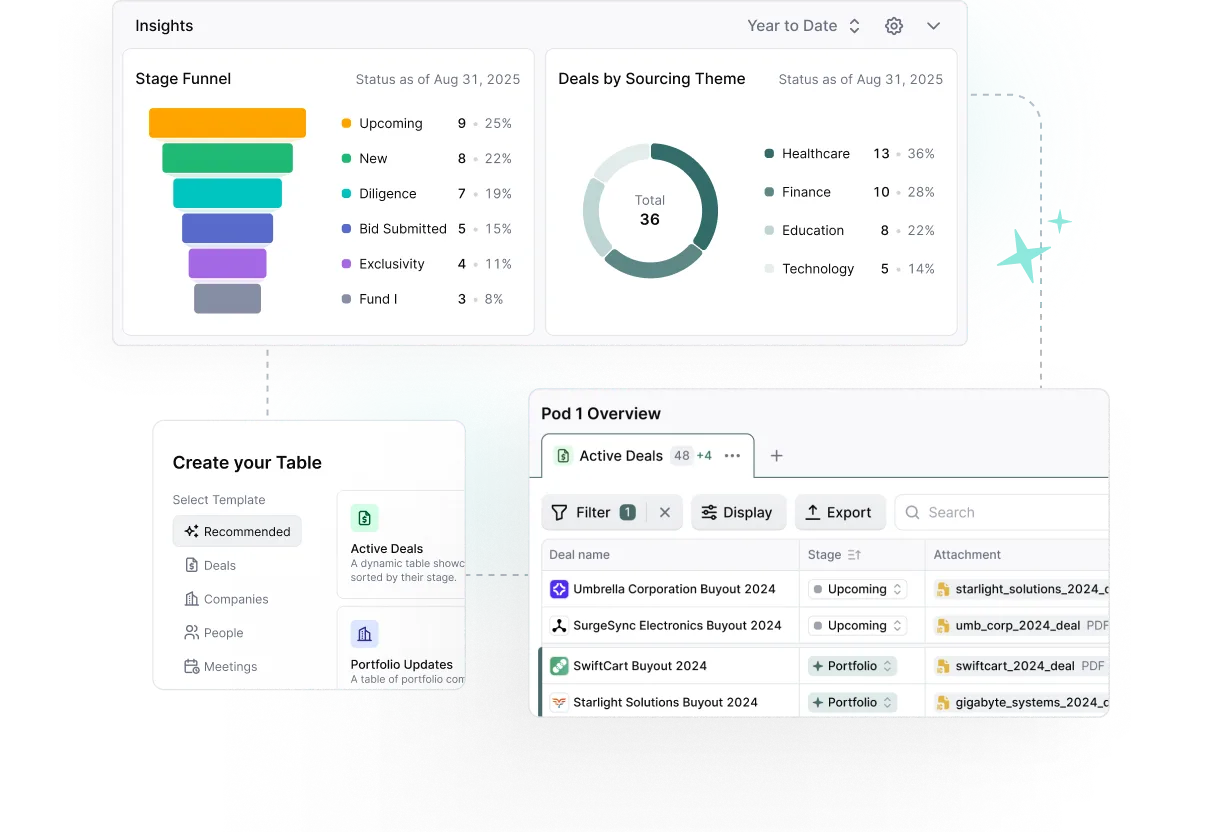

Reporting in private equity and venture capital runs on a cadence, draws from multiple data sources, and breaks down when the underlying data isn't clean.

In private equity, reporting obligations run in two directions simultaneously.

Internally, deal teams are expected to maintain pipeline visibility and attribution discipline.

That data informs how the firm approaches sourcing, and without it, pipeline conversations rely on whoever has the best memory in the room.

Externally, LP reporting in PE is formal and recurring. Quarterly reports covering fund performance, capital account statements, fee and expense disclosures, and valuation marks are standard expectations at the institutional level.

Many LPs, particularly pension funds and endowments, have their own reporting templates they expect firms to complete. The output must be structured data that reconciles back to the fund's own records.

In venture capital, the reporting cadence is less standardized, but no less demanding in practice.

LP updates tend to focus on portfolio company progress:

And LPs want to understand how the firm is thinking about deploying reserves into its best performers, and whether that strategy is holding.

Internally, VC firms track portfolio health metrics across a wider set of companies simultaneously, which creates its own data management challenge.

Keeping company records current across a portfolio of twenty or thirty early-stage businesses requires consistent input from partners and associates, as well as a system that makes that input easy enough to actually happen.

Generic CRMs are built around a sales object model: leads convert to opportunities, opportunities convert to closed deals, and the cycle resets. That logic maps poorly onto either PE or VC workflows, where relationships span decades and deals take years to materialize. The closed event is the beginning of a long ownership or board engagement, not the end of the process.

Which is why a generic CRM can track contacts and log calls, but it can't model a fund lifecycle, attribute deal flow to intermediary relationships, or generate an LP capital account statement. That gap is where private markets firms lose the most operational leverage.

Traditional sales logic maps poorly onto either PE or VC workflows, where relationships span decades and deals take years to materialize. Most importantly, the closed event is the beginning of a long ownership or board engagement, not the end of the process.

And between PE and VC, there are subtle differences that make it important to choose a CRM that’s purpose-fit for exactly what your firm does.

The firms that get the most out of their data stack are the ones whose system of record reflects how they work: where sourcing data connects to portfolio data, LP records connect to fund performance, and reporting pulls from a single trusted source rather than being assembled manually before every investor update.

The foundational objects in a PE CRM are funds, investments, portfolio companies, and LP commitments.

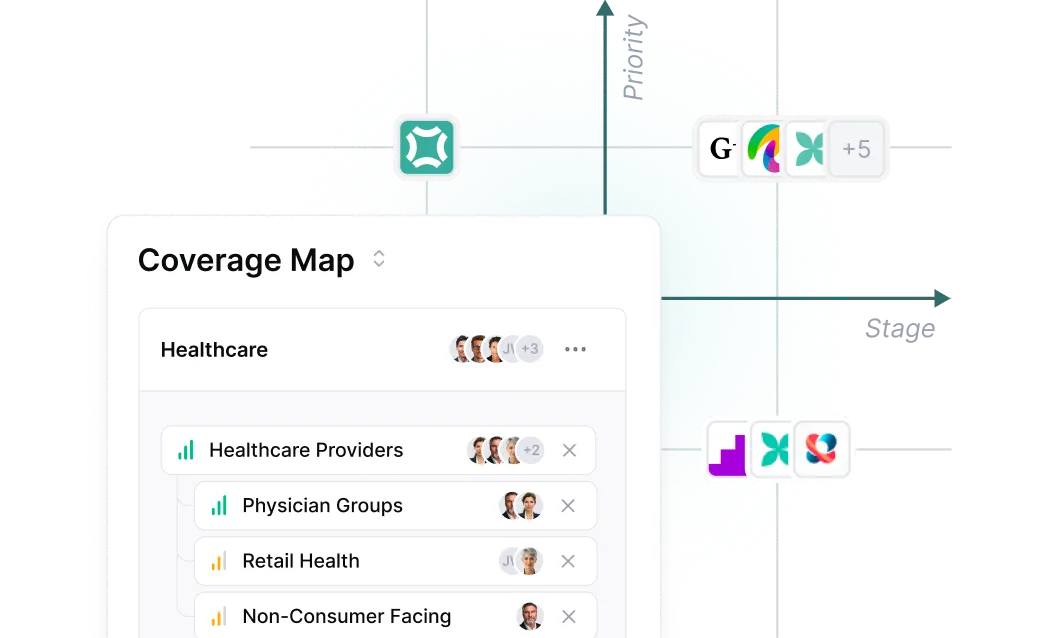

VC firms need to track a higher volume of early-stage relationships across a wider network.

Knowing what to track is only half the equation: the other half is reducing the manual work required to keep those records accurate and current.

In PE, the highest-value CRM automations are around intermediary attribution, pipeline stage progression, and LP reporting generation. Automatically capturing who referred a deal, when it moved stages, and what the outcome was turns sourcing data into a strategic asset over time.

In VC, automation matters most at the top of the funnel and in portfolio monitoring. Auto-logging inbound deal flow, routing introductions, and triggering portfolio update requests on a consistent cadence removes the administrative drag that causes data to go stale.

It should be clear by now that you can't bolt LP commitment tracking onto Salesforce or retrofit intermediary attribution into HubSpot. The data model either supports how your firm works or it doesn't.

Meridian is built around the way private markets firms actually operate. For PE teams, that means fund-level data, intermediary attribution, and LP reporting in a single connected system. For VC teams, it means a sourcing network that compounds over time and portfolio monitoring that stays current without manual effort.

Underpinning both workflows is Scout AI, which handles data extraction from unstructured documents and continuously enriches company and contact profiles. That means your records stay current without your team doing the manual work of keeping them that way.

With Meridian, you get a CRM that was built for private markets, meaning the infrastructure actually fits your business, and not the other way around.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Table of Contents

Compare purpose-built M&A deal management platforms for 2026 and find the right fit for your corporate development team.