Meridian MCP is live! Connect your deal sourcing data directly to Claude

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

Most private markets firms are optimizing a tech stack that's already being replaced, and mistaking the transition for the destination.

A managing director at a mid-market PE firm told me something recently that stuck with me. His firm had just finished a full stack audit. Got the new CRM, AI layer under evaluation, two legacy tools on the chopping block. He was proud of the progress. Then he said, "I think we're finally where we need to be.”

Where his firm landed is better than where they started, but it's not where private markets firms are heading. The technology will undoubtedly evolve in the next 6-18 months.

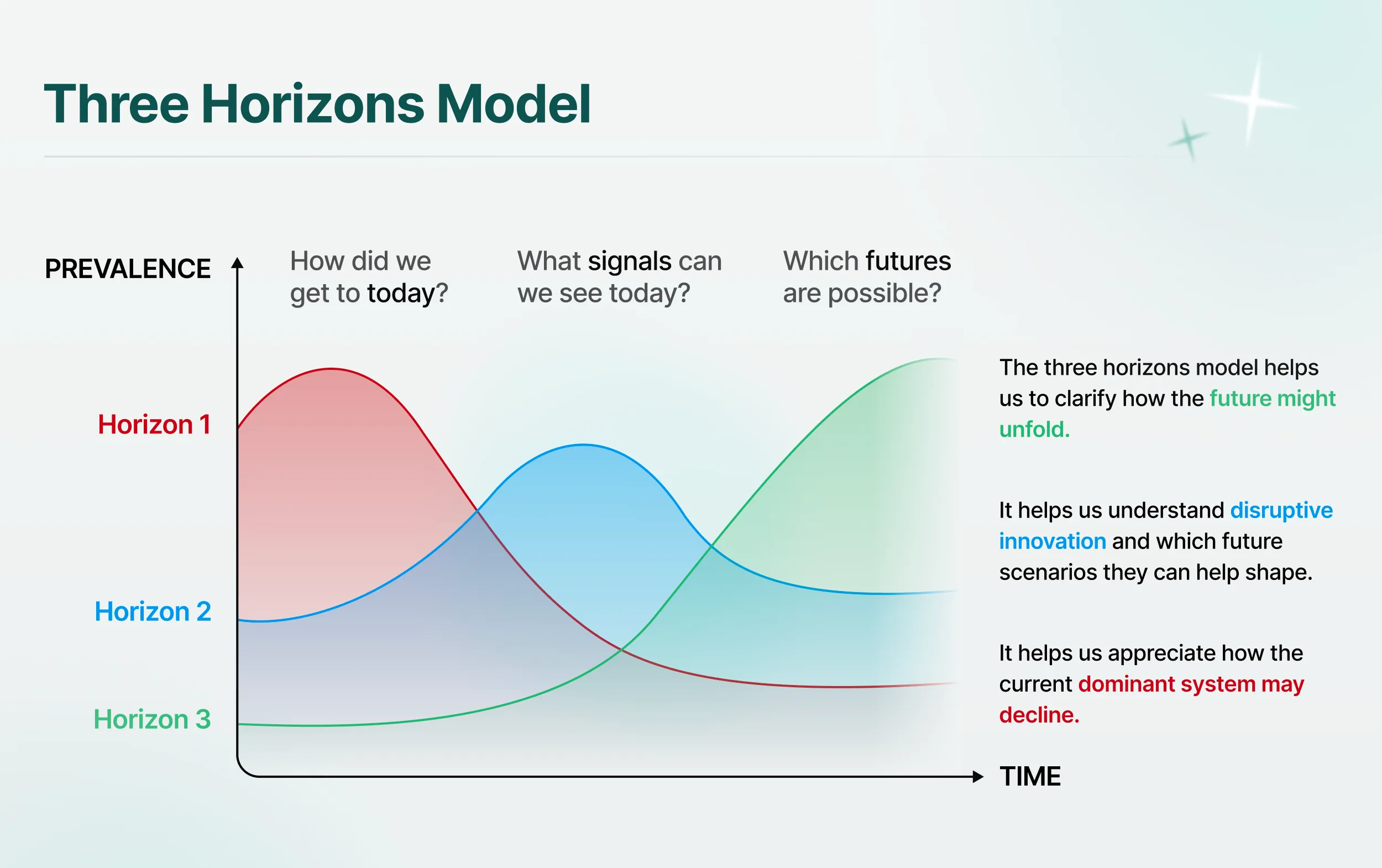

I didn't push back in the moment. But I've been thinking about it since, especially as I've been doing a deep dive on futures thinking through a World Economic Forum program I'm part of this year. One framework keeps coming back to me when I think about private markets tech: The Three Horizons Model.

The Three Horizons model maps how current systems give way to better ones and what gets in the way. H1 is the dominant model today, optimized and running, but gradually losing fit for purpose, even when it doesn't feel that way from the inside. H2 is the transition: new capabilities emerging, old ones fading, everything slightly unstable. H3 is the future model, visible today only at the margins. The critical insight is that all three exist simultaneously. H3 is already being built while most of the market is still living in H1.

Most PE firms are in H1. A fast-growing number are reaching into H2. Almost nobody is building for H3.

The distinction matters because firms that mistake H2 for the destination will spend the next three years optimizing for a model that's already being replaced.

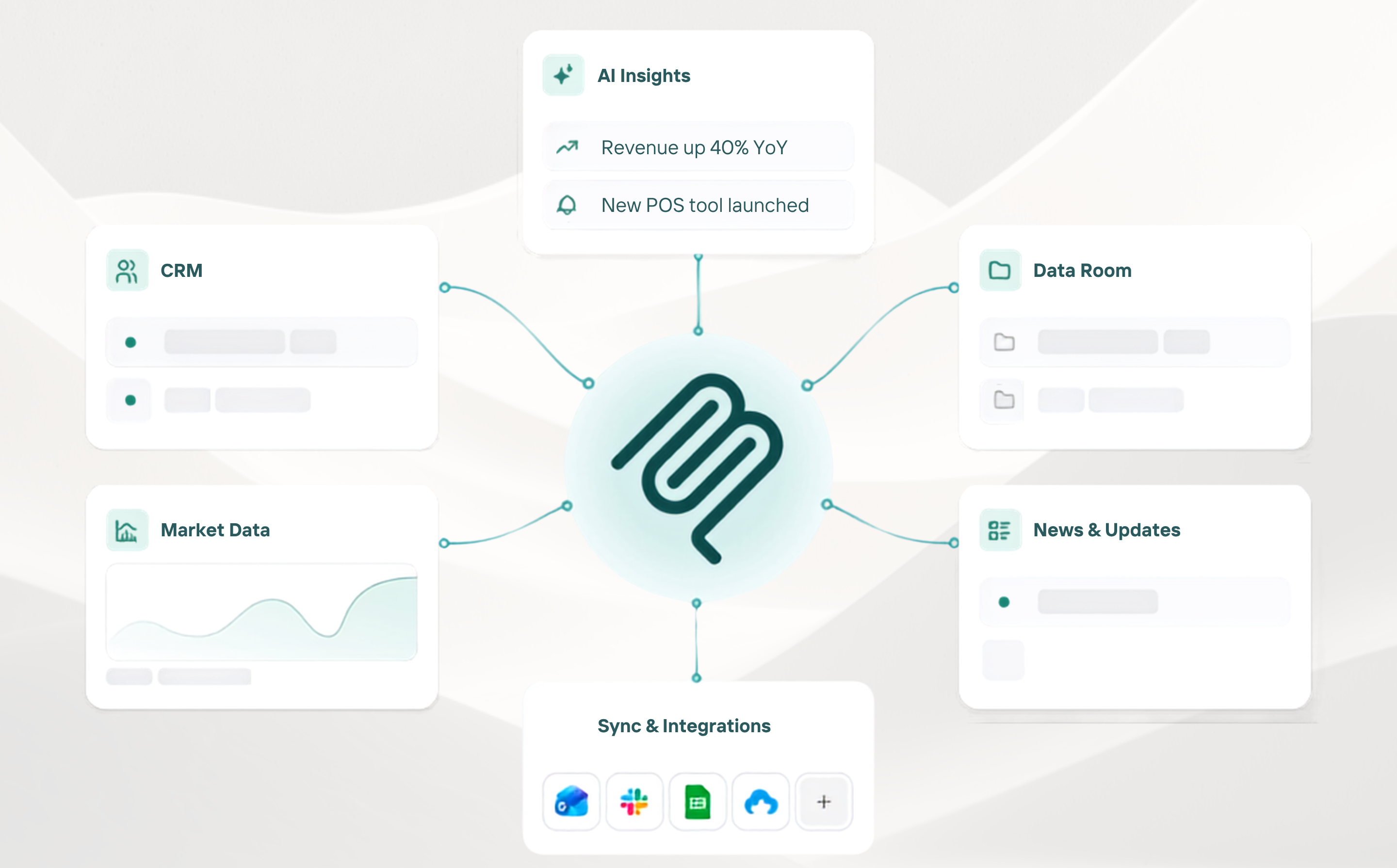

H1 is the DealCloud pipeline, the PitchBook subscription, the Notion diligence tracker, the Slack thread where the real decisions get made. It's the system that mostly works, as long as you don't look too hard at the seams.

The fragmentation problem — or what I've called the integration debt in earlier pieces — is a feature of H1. Every tool solved a real problem when it was bought. The aggregate cost only became visible later. Take context-switching, institutional knowledge trapped in personal inboxes, Zapier workflows breaking silently, etc. as examples.

Most firms spent 2023 and 2024 optimizing H1. Better CRM selection, tighter data hygiene, maybe a cleaner LP reporting setup. That work was real and it mattered. But it's table stakes now. H1 optimization is not competitive differentiation.

The firms I still see stuck in H1 aren't lazy. They're busy. The deal clock doesn't slow down for stack audits.

H2 is where most of the interesting activity is happening right now. It's the AI layer getting bolted onto existing workflows. The MCP-enabled integrations replacing point-to-point connections. The internal AI team hire — the VP of AI & Automation, the SVP of AI Innovation, the Forward-Deployed AI Specialist — standing up capabilities the firm didn't have eighteen months ago.

I wrote about the hiring wave in the last piece. H.I.G., Updata, Vista, and Ares are all firms across the market that are building internal delivery organizations.

But here's the problem with H2: It's structurally unstable. The pattern right now is AI alongside the workflow, not inside it. Export to Claude, get output, paste back in. Run the MCP connector, pull the data, make a decision. The human is still the integration layer between tools.

That's better than H1, but it's not H3.

H2 is also where the talent confusion is happening. EY data shows 51% of PE firms are now hiring data scientists and AI experts. AI and data hiring in PE has increased 38% year over year. The headlines ask whether the associate seat is disappearing. That's the wrong question, and it's a distraction from the more important one: What kind of employee does H3 actually require?

H3 is where the deal team is smaller and sharper.

Not necessarily fewer bodies, but a fundamentally different leverage ratio. In H1, an associate spends the first year rekeying data, pulling comps, and building the first-pass model from a CIM. In H2, AI compresses that from two weeks to two hours. In H3, that work is absorbed entirely by the stack, and the associate walks in on day one expected to do something else.

Meridian's CEO, Alex Sen, wrote about this recently from the individual side. The floor has risen, the ceiling has too, and the associates who thrive in H3 are the ones who can direct AI rather than just use it, who understand that a model grounded in a real system of record is fundamentally different from a model prompted in isolation. He's right about what it means for the person entering the market. The flip side is what it means for the firm building the team.

If the mechanical work is absorbed by the stack, and junior talent is doing VP-level analytical work earlier, then the pyramid doesn't scale the same way. A leaner team with better infrastructure and higher-caliber leverage at every level outperforms a larger team running H1 infrastructure. That's not a prediction; it's already observable at the firms building deliberately toward it.

The other H3 characteristics that aren't getting enough attention:

Institutional memory becomes infrastructure. Why you passed on a deal, what the founder said in the first call, what the comp set looked like when you first saw it — all of it captured, indexed, and surfaced at the right moment by asking the system. This is still mostly unsolved, but the firms getting to H3 will have cracked it.

The COO and the technology function are running the same conversation. Right now, most firms have a technology mandate that sits outside the deal-making function. It reports to the wrong person, gets measured on the wrong metrics, and builds for the workflow that should exist rather than the one that does. In H3, that distinction collapses. Operational infrastructure and investment decision-making are integrated, not parallel.

The stack doesn't have seams. No translation layer. No human bridging between tools. AI lives inside the workflow, and the deal professional interacts with a system that already knows the context.

The BCG and EY research on AI's impact on entry-level finance roles is generating a lot of anxiety in recruiting circles. That anxiety is pointed at the wrong thing.

The associate seat isn't the risk. The risk is firms that keep hiring for H1 while claiming to be building for H3. Associates who arrive expecting to learn the job by doing mechanical work and firms that expect to train them that way are both going to find the gap.

The talent profile that thrives in H3 is different. Written communication and the ability to explain why a deal works in clear, defensible, actual human language are the primary differentiators, not modeling speed. The ability to direct AI effectively, to specify inputs, check outputs, and iterate with judgment rather than just click through a tool, is the new literacy. And understanding what context actually makes AI useful is what will separate the operator from the tourist.

Here's my honest take. Most private markets firms are in H1, reaching for H2, and calling it transformation.

The FTI 2026 PE AI Radar found that while 95% of firms report AI initiatives meeting their business case criteria, talent remains the primary constraint to scaling adoption for 35% of respondents. The gap between "we have an AI strategy" and "AI is native to how we work" is wide and getting wider between the firms moving deliberately and the ones moving reactively.

The Three Horizons framework is useful here not as a destination map but as a diagnostic. Ask yourself where your firm actually is, not where you'd like to be or where you told your LPs you are and you'll have a clearer view of what the next decision actually needs to solve for.

H1 to H2 is a tooling and integration problem. H2 to H3 is a talent and org design problem. They require different answers and different timelines.

The MD who told me his firm was "finally where they needed to be" isn't wrong that the progress was real. He's just thinking about it as a destination instead of a position on a longer arc.

The firms that get to H3 first won't announce it. You'll just notice they're moving faster, deciding better, and not losing people when partners leave.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Table of Contents

The top investment banking CRM and deal management platforms for 2026, compared on automated capture, mandate management, and time to adoption.