Meridian MCP is live! Connect your deal sourcing data directly to Claude

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

Why most investment firm CRM rollouts fail, and the five criteria plus 90-day process that predict which platforms actually get used.

When investment firms ask what they should look for in a private markets CRM, the answer that produces good long-term outcomes is not a feature list, it is a workflow audit. Between 55% and 70% of CRM deployments fail to meet their planned objectives, with poor user adoption as the primary cause. At investment firms, where partners will not manually log activity, and deal data spans years across funds, the failure rate climbs higher. The S&P Global 2026 Private Equity and Venture Capital Outlook found that 64% of PE firms rate their AI tools as ineffective for deal sourcing and 75% rate them ineffective for portfolio monitoring — signs that tool selection is happening without rigorous evaluation criteria.

The firms that avoid this outcome evaluate CRMs the same way they evaluate investments: They define the criteria first and let the evidence drive the conclusion.

This guide provides that framework. It covers the five criteria that predict long-term CRM success at investment firms, a 90-day evaluation process, the specific questions to ask every vendor, the costs beyond licensing that determine total investment, and the red flags that signal a platform is wrong for your firm. This framework applies equally across private equity, venture capital, investment banking, and private credit.

Most private markets CRM implementations fail for one of three structural reasons, each of which is avoidable with the right evaluation process.

For a structural comparison of how sales CRM architecture differs from investment workflow needs, see Private Equity CRMs vs Standard CRMs.

These criteria predict long-term adoption because they map to the structural constraints of investment workflows: deal teams that will not log activity manually, data that spans years and fund vintages, and an information advantage that only compounds when the system is actually used.

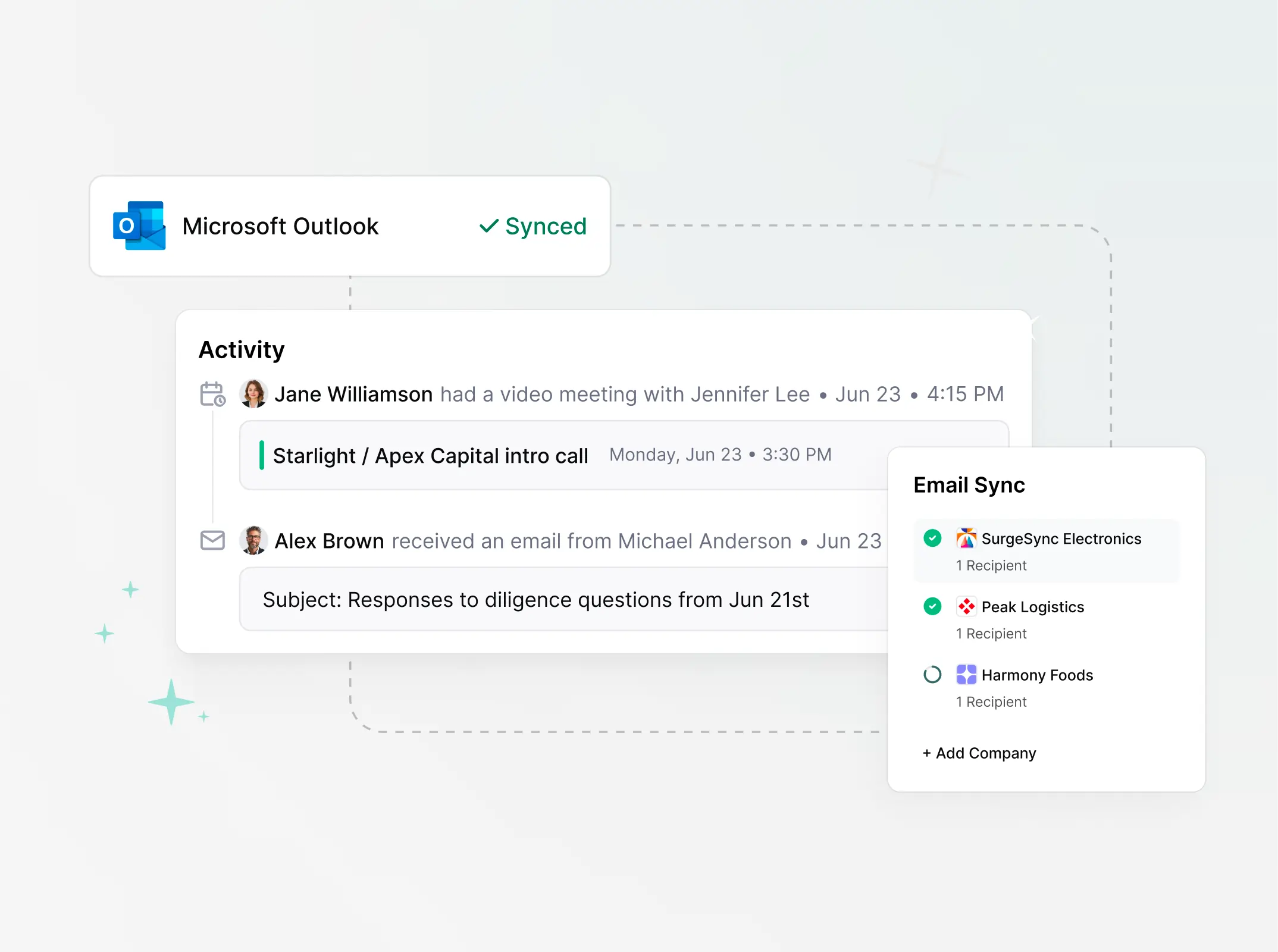

Automated data capture is the single strongest predictor of CRM adoption at investment firms. Platforms that rely on manual entry achieve low, unsustainable adoption; platforms that sync email and calendar interactions automatically — creating and updating records without any user action — achieve meaningfully higher adoption over time.

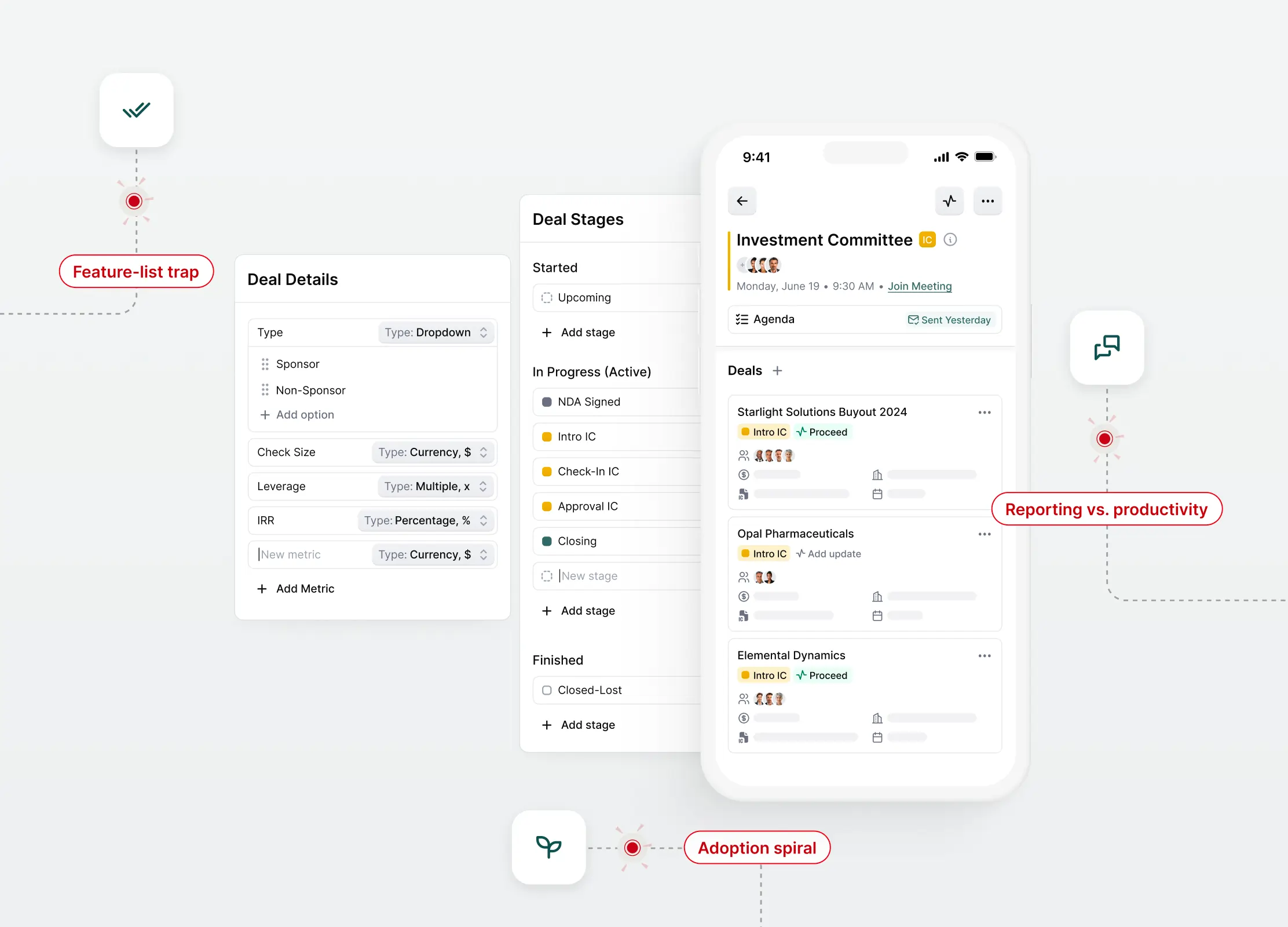

The evaluation test: Ask each vendor what happens when a partner emails a target company CEO three times over two months but never opens the CRM. Does a contact record get created automatically? Does an activity log appear against the correct deal and company records? Does the meeting get linked to the relationship history? Any manual step in this sequence is a data capture gap that compounds over time.

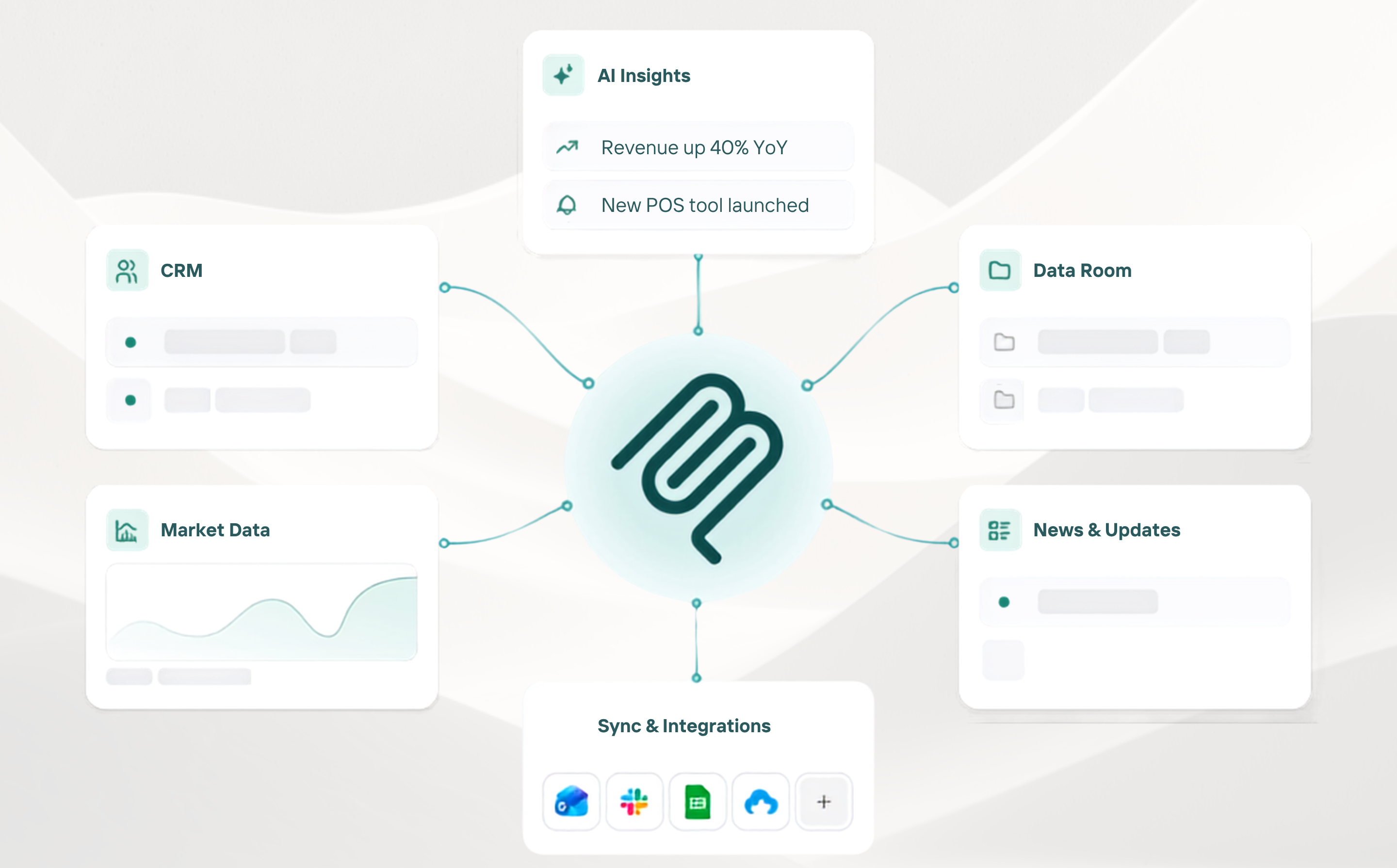

Meridian's Scout AI captures email and calendar interactions automatically, logging them against the correct deal and company records without a manual step. This matters most at the partner level, where relationship data is most valuable and manual logging expectations are lowest.

Generic CRMs model linear sales pipelines. Investment workflows are non-linear, relationship-driven, and span years. A target company may move through sourcing, diligence, IC, portfolio monitoring, and exit preparation over five or more years and appear in deal records across multiple fund vintages simultaneously. A platform that cannot handle this natively requires workarounds that erode adoption.

The evaluation test: Ask the vendor to demo a deal moving through sourcing, initial outreach, diligence, IC submission, and portfolio monitoring. Ask specifically how it handles the same company appearing across two fund vintages. The S&P Global 2026 PE survey found that 60% of GPs cite fragmented data and limited portfolio visibility as a constraint on value creation. The workflow fit problem is widespread.

See also: Private Equity CRMs vs Standard CRMs.

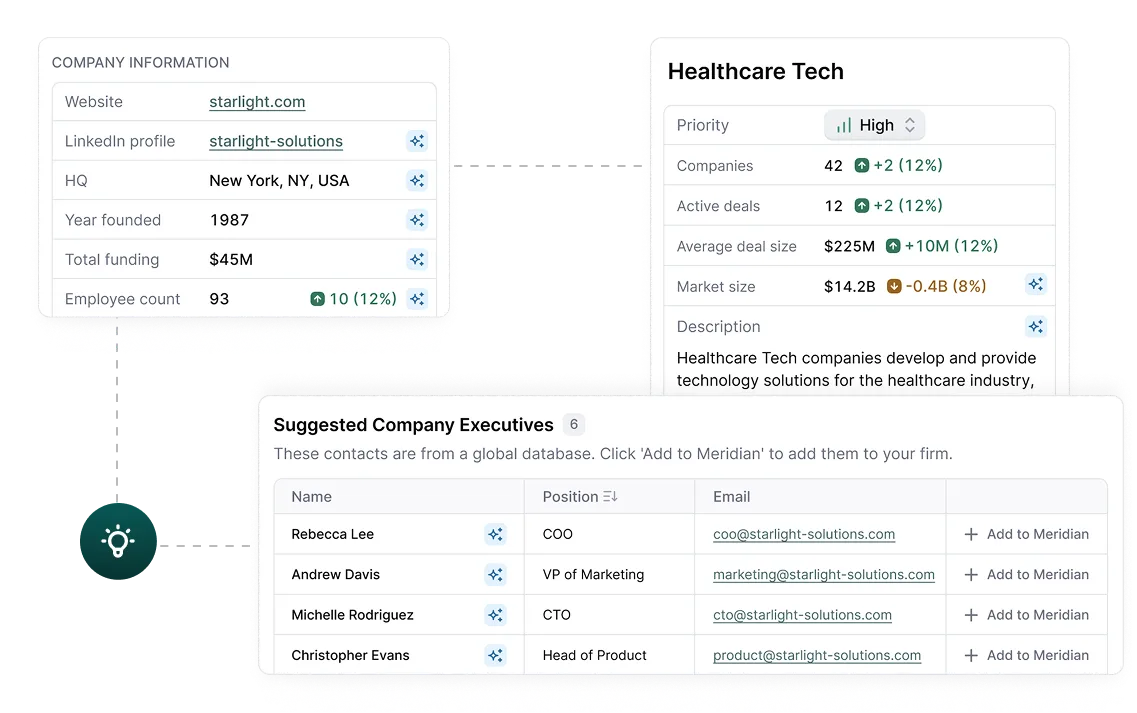

Investment firms need current, accurate data on companies, founders, and markets. Where that data comes from, and how it gets into the CRM, determines how much it costs and how reliable it is.

The bundled model layers the platform's proprietary dataset, third-party integrations, and AI-enriched web crawls into living company profiles that update passively. The unbundled model requires separate PitchBook, Preqin, or SourceScrub subscriptions that sync imperfectly and need ongoing maintenance.

The evaluation test: Ask the vendor if enrichment is included in the subscription or separately priced, and which source wins when two sources disagree on a data field.

Meridian covers 26 million company records with waterfall enrichment and per-field source control included in the subscription, without per-seat data licensing.

Licensing is typically the smallest component of the total investment in a private markets CRM. TCO typically runs two to three times the annual licensing fee once implementation services, data migration, ongoing administration, user training, and integration maintenance are included.

Specialized PE platforms typically take 2 to 6 months for standard configuration; Salesforce requires 3 to 9 months for comprehensive customization; and DealCloud implementations can run up to 6 months for firms with deep customization needs. Each of those months represents internal team time and, often, external consulting fees. Pricing model structure also affects long-term TCO: per-seat pricing scales linearly with headcount, creating budget pressure at every hire.

The evaluation test: Ask the vendor how long an implementation will take for your firm; not just how long the “average” implementation is.

For Meridian implementation scope and timeline details, see Meridian's implementation overview.

Not all CRM AI is architecturally equivalent. Native AI embedded in the data capture and enrichment layer can automate sourcing signals, trigger enrichment runs, surface relationship gaps, and flag portfolio monitoring signals proactively, without a user prompt. Bolt-on AI sits above the database as a chatbot or copilot; it responds to queries but cannot automate the capture or enrichment process itself, which means it operates on whatever incomplete data the system already holds.

Meridian was built by and for PE professionals, providing tools that keep your firm strategic, efficient, and ahead of the game.

The evaluation test: Ask whether the AI feature is included in the standard subscription or separately priced. Ask whether it can act on data proactively or if it only responds to explicit queries. PwC's survey of PE executives found that 50% believe generative AI and agentic AI will have the most transformative impact on their industry over the next three years. The S&P Global 2026 survey found that 64% of firms rate AI as ineffective for deal sourcing and 75% rate it ineffective for portfolio monitoring. The gap between expectation and result is largely an architecture problem.

Define your CRM requirements before watching demos, use structured vendor tests rather than default demo flows, and measure adoption data rather than user sentiment during pilots. The following five-phase process reflects what we see work in practice.

Visual representation of the project process flow, highlighting sequential steps and their interrelations.

Include a partner, an associate, and an operations lead.

An evaluation team missing any of these roles will optimize for the wrong outcome.

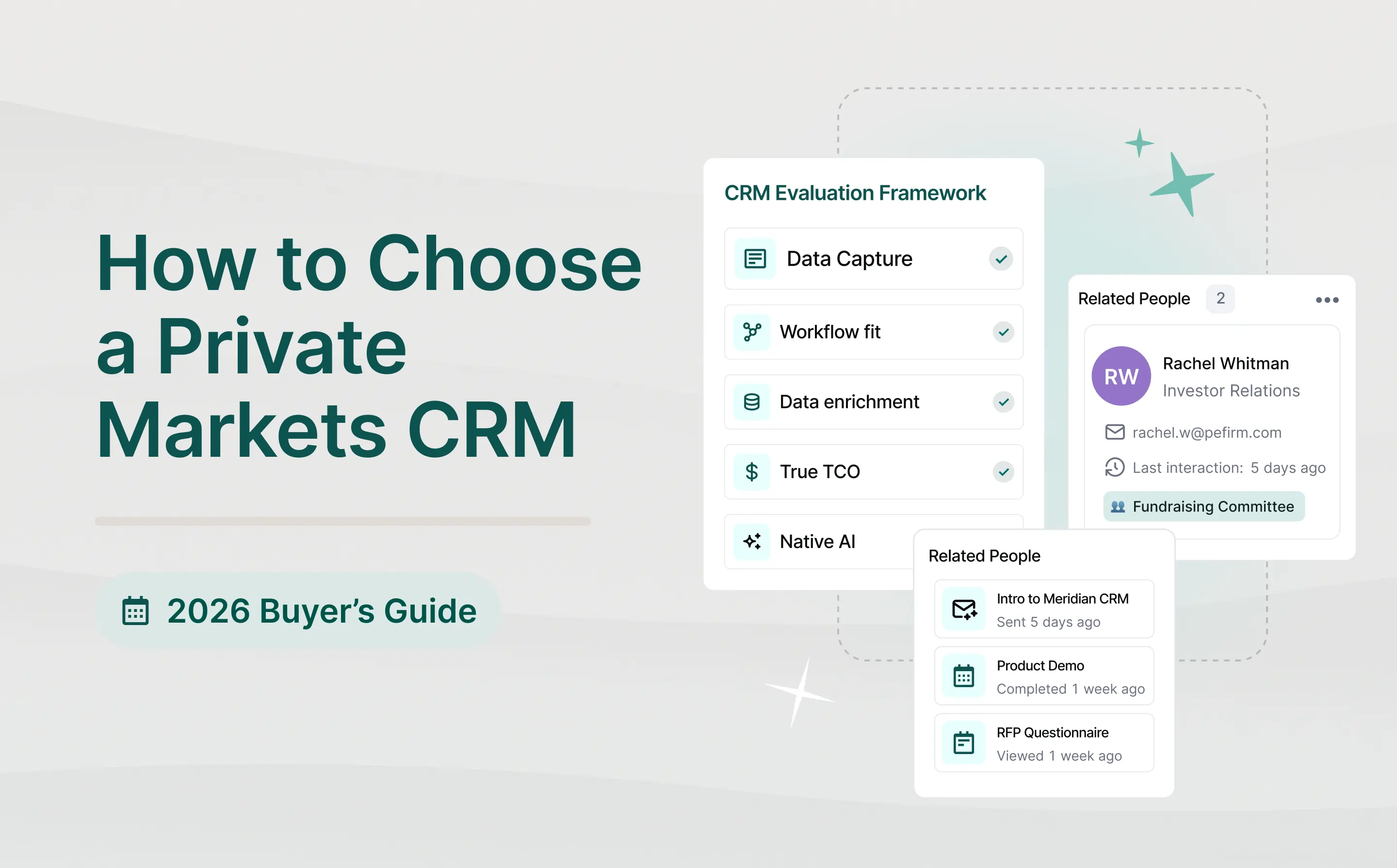

List the five workflows the platform must handle without workarounds, then rank them. These ranked requirements are the evaluation criteria. Not the vendor's capability matrix, but the five things the platform must do, in the order they matter to your team.

Shortlist three to four platforms. Ask each vendor to demo your ranked workflows using real or representative firm data. A vendor who cannot demo against your actual use cases with realistic data is signaling something about the product's maturity.

Get references from firms of similar size and strategy. Ask each reference how long implementation actually took, what adoption looks like today versus 90 days post-launch, and what they would do differently. The adoption question is the most revealing.

Measure adoption and data quality, not user sentiment. If active usage is not above 80% at 60 days post-launch, investigate the specific workflows creating friction before attributing the problem to change management.

These questions surface the differences that matter most to private markets firms in daily practice. Use them to structure every demo and reference call.

For Meridian's security and compliance posture, see Security Overview.

The vendor cannot provide a specific implementation timeline for your firm size. A vendor that can only provide a wide range, or describes implementation as inherently unpredictable, is signaling an immature onboarding process.

Every demo runs on sanitized sample data. A platform that handles real deal data well should be able to show it. If the vendor cannot demo against realistic firm data in the sales process, that constraint will follow you into implementation.

The AI feature is separately priced and described as a copilot. Bolt-on AI that answers questions about existing data is a different product from native AI that automates capture and enrichment.

Reference customers are larger or structurally different from your firm. A reference at a 200-person multi-strategy fund provides little signal about fit for a 20-person sector-focused PE firm. Ask specifically for references that match your headcount and investment strategy.

The pricing model scales per seat with no ceiling. Per-seat models create a CRM budget discussion at every new hire. This compounds quickly at the associate and analyst levels, where headcount grows fastest and where broad access adds the most operational value.

The vendor describes manual data entry as a best practice for data quality. This frames an architecture limitation as a preference. Automated capture systems achieve high adoption rates precisely because they remove the manual burden, and they do so without sacrificing data completeness.

CRM selection is a strategic decision, not a procurement exercise. Evaluate CRMs on workflow fit, data capture method, and total cost of ownership, not demo quality and feature counts. The failure rate for CRM deployments runs between 55% and 70% across industries, and it’s higher at investment firms. That failure rate is not a software problem; it is an evaluation problem.

The five criteria in this guide predict long-term adoption because they map directly to private markets firm constraints: senior professionals who will not log activity manually, deal data that spans years and fund vintages, and an institutional memory that only compounds when the system is actually used. A platform that scores well on all five will be used widely by a firm. One that does not will be abandoned, regardless of its feature set.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Make confident, data-driven decisions to close the right deals and improve investment outcomes.

What should a private equity firm look for in a CRM?

A private equity firm should evaluate CRMs on five criteria: automated data capture method, private markets workflow fit, bundled versus separate data enrichment, total cost of ownership beyond licensing, and AI architecture. Between 55% and 70% of CRM deployments fail to meet their planned objectives, with poor user adoption as the primary cause — these five criteria are the strongest predictors of whether adoption will hold at an investment firm.

How long does CRM implementation take at an investment firm?

Specialized PE platforms typically take 2 to 6 months for standard configuration; Salesforce requires 3 to 9 months for comprehensive PE customization; DealCloud implementations can run up to 6 months for firms with deep customization needs. AI-native platforms built specifically for private markets generally onboard faster, with white-glove data migration included. The wide range reflects variation in existing data quality, headcount, and CRM complexity.

Is Salesforce a good CRM for private equity?

Salesforce can work for private equity but requires 3 to 9 months of customization to match investment workflows, plus dedicated internal admin resources to maintain that configuration. For firms with existing Salesforce infrastructure and an established admin function, it is a defensible choice. For firms prioritizing fast deployment and private-markets-native workflows without an ongoing admin burden, purpose-built platforms are a more direct path.

What is the total cost of ownership for a private markets CRM?

Total cost of ownership for a private markets CRM typically runs two to three times the annual licensing fee once implementation services, data migration, ongoing administration, user training, and integration maintenance are included. Per-seat pricing models also scale linearly with headcount, creating recurring budget pressure as the firm grows.

Table of Contents

The top investment banking CRM and deal management platforms for 2026, compared on automated capture, mandate management, and time to adoption.