Meridian MCP is live!

Connect your deal sourcing data to any AI tool.

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

A comprehensive private credit data stack now runs well into six figures a year, and most firms still have stale records. The fix isn't another vendor, it's a different architecture. Here's the framework.

TL;DR

Private credit had already grown into a $3 trillion asset class at the start of 2025, up from roughly $2 trillion in 2020, but the deal data infrastructure supporting it has not kept up. Most firms still manage borrower records through periodic spreadsheet exports from PitchBook or Capital IQ; manual data entry from CIMs and quarterly financial packages; and disconnected systems where deal information lives in one tool, borrower financials in another, and covenant compliance in a third.

The result is stale records, covenant surprises, and missed refinancing signals. Allvue's back-tested covenant monitoring research shows that when a borrower's leverage percentile jumps by 25 points or more over two consecutive quarters, there is a 67% chance of covenant breach within a year. Most firms lack the monitoring cadence to catch that drift before it becomes a problem.

What data enrichment actually works best for private credit CRMs is a continuous, AI-driven, multi-source waterfall model embedded directly in the platform where deal and portfolio decisions get made. Not a quarterly spreadsheet export. Not a single-provider API with coverage gaps. Not a chatbot reading stale fields.

This guide covers what that looks like in practice. You’ll learn how a system of record designed for private markets investing maps enrichment to each stage of the credit lifecycle, compares the major data providers, and lays out a framework any private credit firm can use to build an enrichment strategy that scales with portfolio complexity.

Data enrichment in a private credit context is the ongoing process of enhancing CRM and portfolio records with verified, timely information from internal and external sources across the full credit lifecycle. The definition matters because most content that uses the term treats enrichment as a generic B2B marketing function.

Credit enrichment is something else entirely.

Private credit data enrichment is distinct from private equity and venture capital data enrichment in four ways. It requires:

There are six categories of enrichment that a private credit firm needs to get right. Each sits in a different part of the CRM and pulls from a different source mix.

1. Borrower data

Company financials (revenue, EBITDA, margins, cash flow), credit history and PAYDEX scores from Dun & Bradstreet's 500 million-plus business record database, management profiles, firmographic data, and ownership structure. Middle-market borrowers have the thinnest public data footprints in the economy, which makes this the hardest category to enrich reliably. Federal Reserve research on private credit characteristics shows that average private credit loan sizes have exceeded $80 million since 2022, financing companies that often have limited tangible collateral and no public disclosure requirements.

2. Credit metrics and risk data

Leverage ratios, DSCR, interest coverage, liquidity metrics, probability of default scores from Moody's RiskCalc or similar models, and peer benchmarks by industry and size. This is the category where real-time tracking matters most. A leverage ratio that was fine at closing can look very different four quarters later, and the firms that catch the drift early outperform the firms that catch it at the next reporting cycle.

3. Covenant tracking data

Financial maintenance thresholds, reporting deadlines, compliance status, headroom calculations, and the amendment or waiver history. This data lives inside credit agreements that are drafted deal-by-deal. Structuring it requires either a team of analysts reading PDFs or an AI extraction layer that can parse covenant terms from unstructured legal text.

4. Portfolio company monitoring

Periodic financial updates from borrowers, operational KPIs, cash flow metrics, valuation inputs, and market signals that affect borrower health. The cadence here depends on the loan structure, but for leveraged borrowers a monthly refresh is closer to the right frequency than a quarterly one.

5. Deal flow and pipeline enrichment

Market opportunity sizing, sponsor track records, comparable transaction data, CIM-extracted metrics, and thematic sourcing signals. Credit teams that source from sponsor relationships need this data to move fast on new opportunities without re-running the same diligence work from scratch each time.

6. Contact and relationship data

Verified contacts, interaction history auto-captured from email and calendar, relationship strength scoring, warm introduction paths, and job change alerts. In private credit, the sponsor and lender ecosystem is small enough that relationship intelligence compounds quickly for firms that track it systematically.

Context worth reading: Vantage Point's guide to data enrichment in private credit frames the borrower universe as one of "deliberate opacity," which is the clearest short description of why this problem is so hard for credit firms in particular.

Private credit firms often inherit CRM patterns from PE, VC, or generic sales tools. The pattern does not survive contact with a credit portfolio, and the reasons come down to three structural mismatches.

Frequency

PE and VC firms can refresh company data quarterly because the questions they ask of that data are strategic and long-horizon. Credit teams cannot. Borrower financials change between reporting periods, covenant compliance windows are tight, and credit deterioration can accelerate inside a single quarter. A CRM that refreshes on a calendar cadence will always be behind the risk that matters.

Data types

Standard enrichment providers like ZoomInfo and Clearbit were built to enrich contacts and companies for prospecting. Credit CRMs need something different: borrower-level financials (EBITDA, leverage, coverage ratios), structured covenant data extracted from loan agreements, and collateral and recovery data. None of that exists in generic B2B data. Even the larger financial data providers vary widely in how deeply they cover middle-market private borrowers, which means most credit firms end up stitching multiple sources together to close coverage gaps.

Opacity of the borrower universe

This is the mismatch that generic tools cannot solve by getting better. Private credit borrowers are overwhelmingly structured as private LLCs and LPs with no public disclosure requirements. Standard enrichment was built for public companies and VC-backed startups with Crunchbase profiles. A middle-market direct lending borrower is neither. Enrichment for this universe has to be assembled from sponsor reporting, D&B records, sector-specific databases, news and filings monitoring, and whatever the firm's own analysts have gathered in diligence. That is a different kind of data problem, and it does not bolt onto a sales CRM.

The fastest way to scope an enrichment strategy is to map it against the stages of the credit lifecycle. Each stage has different data needs, different source mixes, and different freshness requirements. A framework that works for origination does not work for portfolio monitoring, and vice versa.

The practical takeaway from this mapping is that no single data provider covers the whole lifecycle. A credit firm relying on one vendor will always have coverage gaps in either origination, underwriting, or monitoring. This is why the best enrichment strategies assume multiple sources from the start rather than trying to stretch a single source across stages it was not built for. For the deal sourcing end of the workflow specifically, it is worth reading our companion piece on deal flow management with AI.

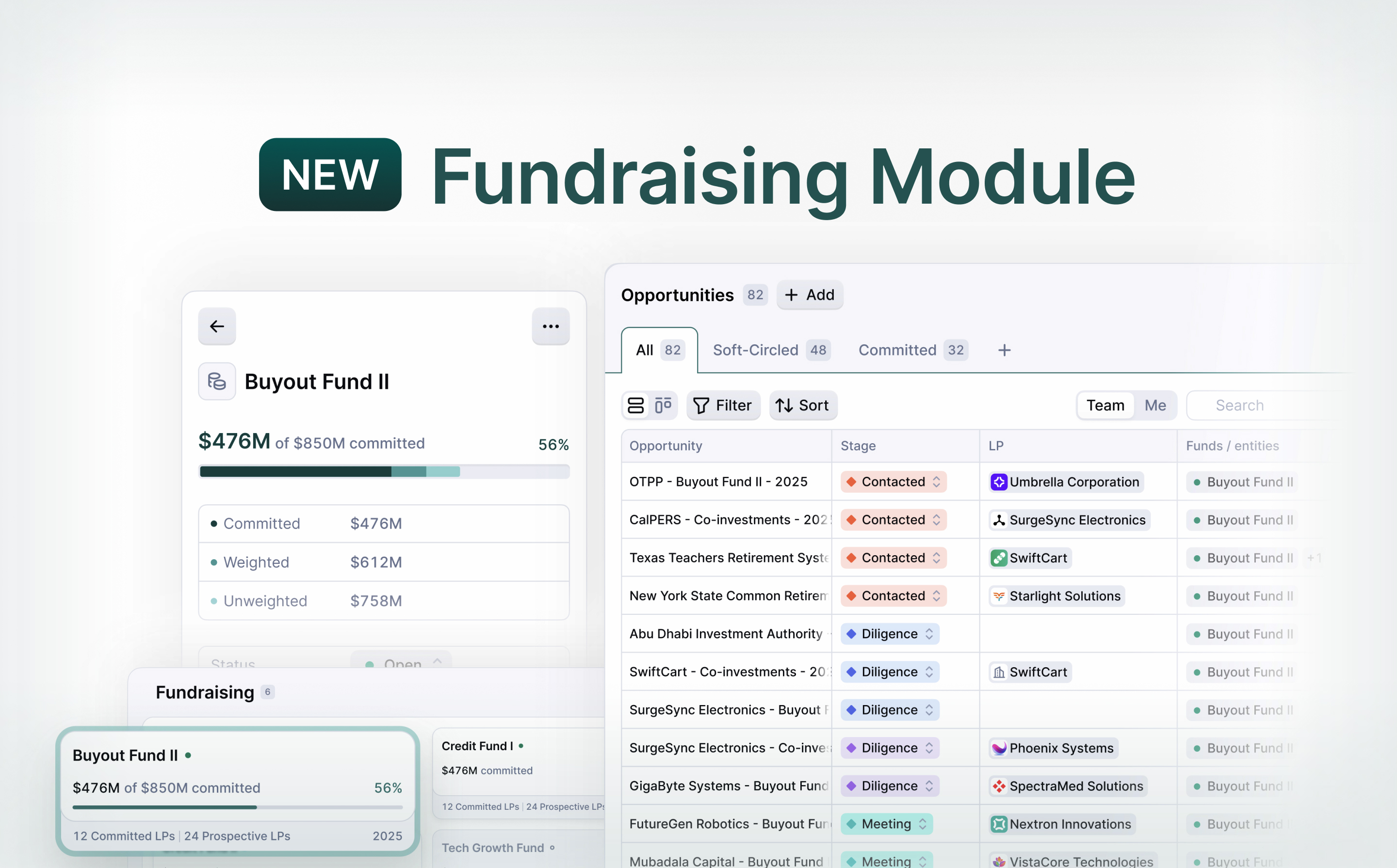

There are three enrichment models in use today at private credit firms. They coexist in the market, and firms often use a combination, but the end state worth building toward is clear.

Approach 1: Manual and periodic imports

The analyst exports data from PitchBook, Capital IQ, or a spreadsheet and uploads it to the CRM on a schedule (monthly, quarterly, ad hoc). This is the most common pattern at firms under $2 billion AUM. It is cheap, familiar, and requires no new infrastructure. It also guarantees stale records, consumes analyst time that should be spent on credit judgment, and breaks every time a data export format changes. The cost is real but distributed, which is why it persists longer than it should.

Approach 2: Single-source API integration

The CRM connects to one primary data provider, typically PitchBook or S&P Capital IQ, via API. Data refreshes on a defined cadence rather than by analyst action. Freshness improves, manual work drops, and the CRM starts to feel like a system of record rather than a filing cabinet. The trade-off is single-source dependency. No single provider covers the full private credit universe, and middle-market borrowers in particular fall through coverage gaps. Firms on this model end up supplementing with spreadsheet imports for the borrowers their primary vendor does not track well.

Approach 3: Waterfall enrichment

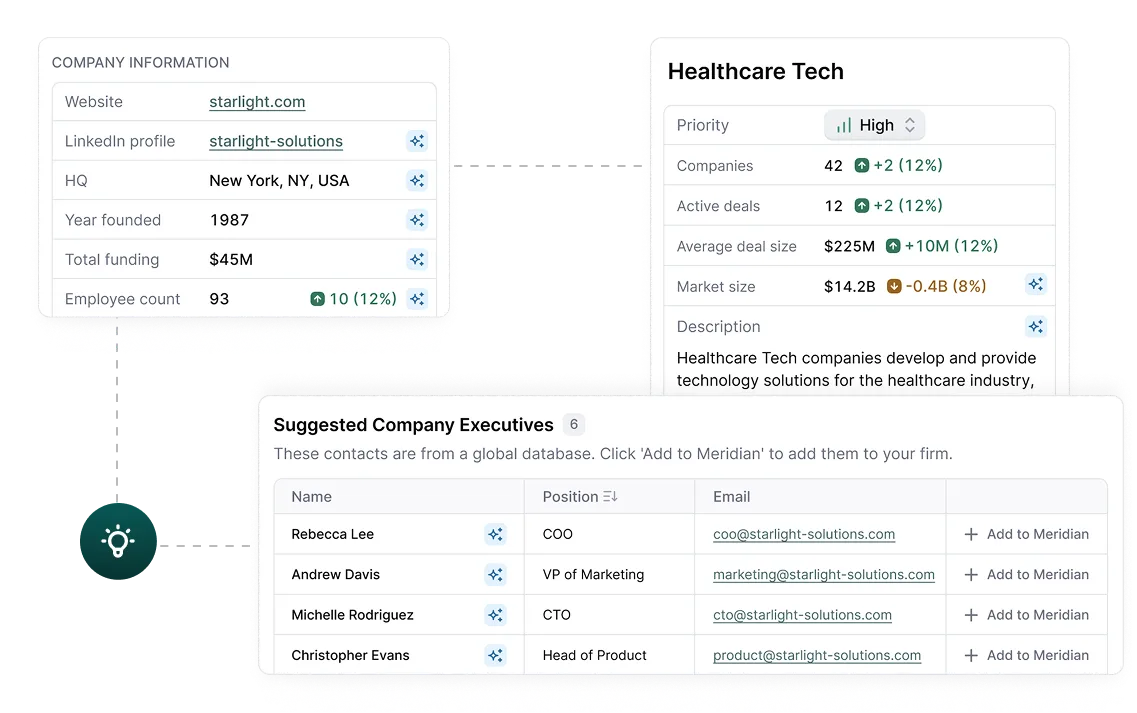

The CRM checks multiple data sources in a prioritized hierarchy. For each field on a borrower record, it pulls from Source A first, falls through to Source B for missing fields, supplements with Source C, and overlays the firm's own proprietary data (emails, meeting notes, CIM extracts) as the top-priority layer. The firm controls the hierarchy. Coverage gaps shrink because sources complement each other rather than overlap. Proprietary data stays on top, which means the firm's own analyst work is treated as the authoritative source rather than getting overwritten by generic vendor data.

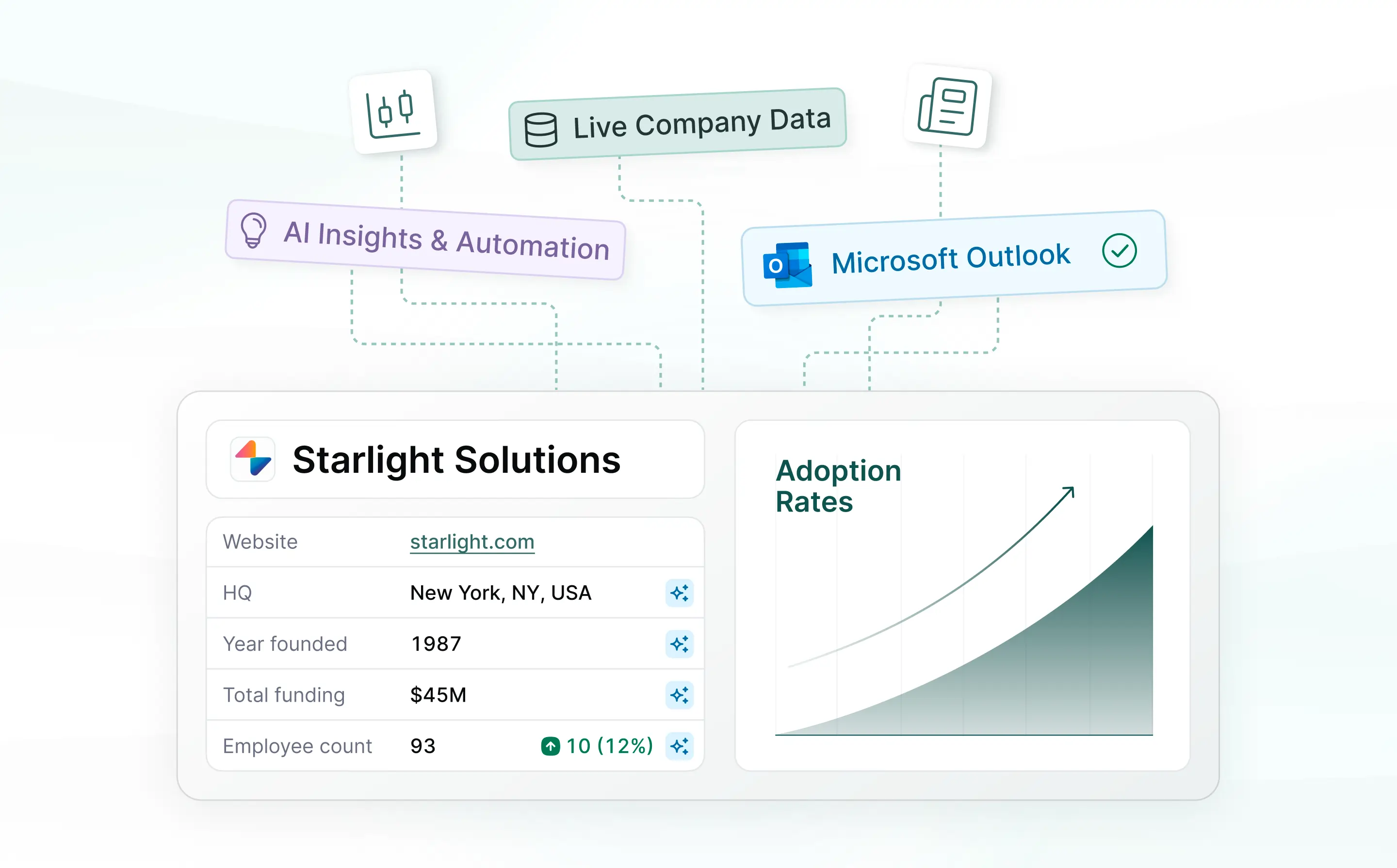

Waterfall enrichment is the model our platform runs on, which is why we have a direct view of how it plays out in practice. The base layer is 26 million company records bundled directly into the CRM. On top of that, firms configure integrations with PitchBook, SourceScrub, Grata, Crunchbase, and any other data source they rely on, in whatever priority order they choose. Their own proprietary data (notes, emails, CIM extracts) sits at the top of the stack and is treated as authoritative. Several of our customers have been able to reduce per-seat PitchBook licenses after onboarding because the bundled data covers the majority of their enrichment needs, though firms with heavy leveraged-loan comparables work still tend to keep PitchBook for LCD data specifically.

The honest trade-off for us: Waterfall enrichment takes more initial configuration than a single-source integration. Firms that want a plug-and-play connector to one vendor can stand up Approach 2 faster. We take the view that a week or two of setup at the start pays back many times over in a portfolio that spans hundreds of borrowers, but that is a bet each firm has to make for itself. See our data enrichment product page for how we implement the hierarchy.

Meridian was built by and for PE professionals, providing tools that keep your firm strategic, efficient, and ahead of the game.

Whatever enrichment architecture a firm chooses, the underlying data has to come from somewhere. These are the providers that show up most often in private credit data stacks, and what each is actually good for.

PitchBook

Strongest on deal and transaction data, fund performance, and sponsor track records. PitchBook's LCD data is widely used for leveraged loan and private credit benchmarks. The platform acquired Lumonic to expand into private credit portfolio monitoring, which signals where the roadmap is headed. PitchBook has also announced integration partnerships with Anthropic, Perplexity, Rogo, and Hebbia to embed its data into AI workflows, which is worth tracking if AI-assisted research is part of the firm's workflow. Pricing is enterprise-scale and scales with users, which pushes firms with large teams to evaluate whether they need full seats for every analyst or whether a bundled CRM-plus-data solution makes more sense.

Preqin

Strongest on fund-level data, LP data, and fund benchmarking. Preqin was acquired by BlackRock in March 2025 for approximately $3.2 billion, a move that signals the strategic value of private market data at the asset manager level. Preqin is critical for LP reporting enrichment and for benchmarking fund performance against peers, and it is the most commonly cited source in fundraising workflows for private credit.

S&P Capital IQ

Deep financials on larger, rated borrowers, plus credit ratings data and structured covenant information. Coverage thins out in the middle market, which is where most direct lending activity happens, so firms typically pair Capital IQ with a middle-market-focused source. Capital IQ is usually the right anchor for firms whose book is weighted toward upper-middle-market and sponsor-backed transactions.

Dun & Bradstreet

The D&B Data Cloud covers more than 500 million business records with PAYDEX payment-history scores. Essential for borrower creditworthiness assessment in the middle market. The broadest coverage of private, middle-market companies of any commercial data source, which makes it a common gap-filling layer in a waterfall setup.

Moody's Analytics

Probability-of-default models and RiskCalc scores for private firms. Specialized credit risk output that most other providers do not replicate. Typically an enterprise-tier subscription, and most often used by larger credit platforms that run quantitative risk models in parallel with analyst-driven underwriting.

Emerging private credit-specific providers

A newer category of tools is building specifically for private credit workflows. Allvue Systems recently launched Private Credit Intelligence, covering more than 200 KPIs across deals, facilities, borrowers, transactions, and covenants. Lumonic, now part of PitchBook, automates borrower financial tracking. ScaleX Invest focuses on covenant metrics, PIK ratios, and probability of default calculations specifically tuned for direct lending. These providers do not replace the major vendors, but they are filling credit-specific gaps that the generalist platforms have historically under-served. Allvue's research on private credit transparency and benchmarking is a useful primer on where the category is heading.

The cost reality: a comprehensive data stack for a mid-size private credit firm (PitchBook plus Preqin plus Capital IQ plus D&B plus CRM plus a monitoring layer) can run well into six figures annually. This is the economic pressure driving consolidation. Firms are asking whether they need every standalone subscription or whether a platform that bundles a meaningful subset of this data can replace multiple licenses. The answer is firm-specific, but the question is increasingly hard to avoid.

Every CRM vendor in the market has added an AI feature in the last eighteen months. Most of these features are bolt-on. A smaller number are structural. The difference matters for credit firms in particular because credit workflows depend on the underlying data being correct, and bolt-on AI does nothing to improve the underlying data.

Bolt-on AI

Definition: A chatbot or copilot layered on top of a CRM that was not designed for it. The AI can summarize records, generate emails, or answer questions about data already in the system. It cannot enrich, validate, or maintain the underlying data. If a borrower record says EBITDA is $50 million but the latest financial package says $38 million, the chatbot has no idea. This is the architecture most legacy CRMs are working with today, including the Salesforce-plus-Einstein and DealCloud-plus-Intapp Assist configurations. The AI layer is useful for summarization and drafting, but it does not close the data quality gap that creates risk in the first place.

AI-native enrichment

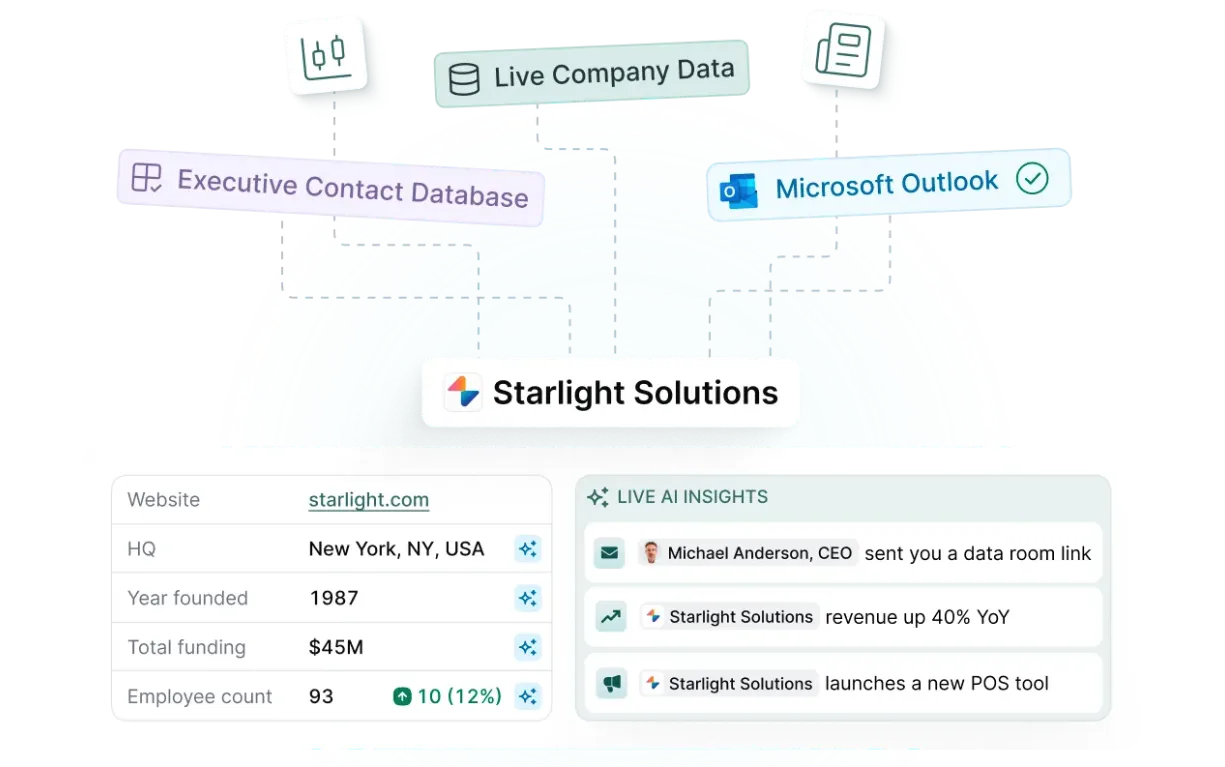

Definition: AI agents that are part of the platform's core architecture rather than bolted on top of it. They crawl the open web for borrower signals (press releases, hiring patterns, regulatory filings), extract KPIs and covenant terms from uploaded CIMs and financial packages, cross-reference multiple data providers to validate and fill gaps, and update borrower profiles continuously without a user triggering them. The AI creates and maintains the data layer rather than just querying it.

What this means for a credit analyst's day

With bolt-on AI, an analyst opening a borrower profile sees whatever was entered at the last manual update, plus whatever the chatbot can infer from those stale fields. With AI-native enrichment, the analyst sees a living profile that reflects the latest available information. Covenant headroom recalculates as new financials flow in. Distressed signals surface before the next quarterly reporting cycle. Our platform uses Scout AI agents to deliver this model, where enrichment runs continuously in the background rather than waiting for a user to click a button. More context on where this is heading is in our post on the future of private equity CRMs, which covers the same architectural shift applied to PE workflows.

Every firm evaluating a CRM is effectively also evaluating an enrichment approach. The two are inseparable. These are the platforms that come up most often in private credit CRM conversations and how each handles enrichment.

A fair reading of this comparison is that every platform is moving in the direction of richer, more automated enrichment, and the differences are in architecture rather than intent. Firms that want a Salesforce-native experience will pick differently from firms that want an AI-native platform purpose-built for private markets. Firms that need deep LCD and sponsor-track-record integration will weight PitchBook depth heavily. The right platform is the one whose architecture matches how the firm actually works, not the one that scores highest on a feature checklist. Our companion piece on the best private equity CRM tools covers the PE-side equivalent of this comparison for firms that run both PE and credit strategies.

Any private credit firm can build a better enrichment setup regardless of which CRM it currently runs. The framework below is CRM-agnostic. Run the six steps in order.

1. Audit your current data quality

Before adding enrichment sources, map what you already have. Pull the fields across your CRM, portfolio monitoring tools, and spreadsheets into one view. Identify stale records (data older than 90 days), empty fields (missing EBITDA, missing covenant terms), and conflicting data (different revenue figures across systems). A useful benchmark: Allvue's 2026 GP Outlook Survey found that 92% of firms describe their data as only moderately organized or worse. If your firm is in that majority, the audit alone tends to surface the highest-priority fixes.

2. Map enrichment needs to lifecycle stages

Use the lifecycle table above. Not every stage needs the same data or the same freshness. Origination can tolerate quarterly firmographic data. Portfolio monitoring for a leveraged borrower needs monthly or real-time financial updates and real-time covenant compliance tracking. Match enrichment investment to where data gaps create the most risk. Spending on high-frequency enrichment for a buy-and-hold subordinated loan is overkill; underspending on high-frequency monitoring for a stressed borrower is expensive in a different way.

3. Choose a source hierarchy, not a single source

No single data provider covers the full private credit universe. Build a waterfall. Pick a primary source for each data category (firmographics, financials, credit, covenant, contact), a secondary source for gap-filling, and treat your firm's own proprietary data (notes, emails, CIM extracts) as the top-priority layer. The CRM has to support configurable source priority for this to work. If it does not, that constraint will become the bottleneck.

4. Automate extraction from unstructured documents

Private credit generates an enormous volume of unstructured data: CIMs, credit agreements, financial packages, covenant compliance certificates, quarterly operating updates. Firms that manually extract data from these documents are creating bottlenecks that scale with portfolio size. Look for CRM platforms with AI or NLP extraction capabilities that can structure this data automatically. This is the single highest-leverage operational change a credit firm can make in 2026.

5. Measure enrichment coverage and freshness

Track two metrics. Coverage rate: the percentage of borrower records with complete fields for each enrichment category. Freshness score: the percentage of records updated within target windows. Reasonable targets are 90%-plus coverage for active borrowers, 30-day freshness for financial data, and real-time for covenant compliance status. Build a simple dashboard for these metrics and review it monthly. What gets measured gets maintained.

6. Consolidate where the economics make sense

A comprehensive third-party data stack easily exceeds six figures annually for a mid-size firm. Before renewing every standalone subscription, evaluate whether the CRM platform's bundled data can replace one or more licenses. Several firms have been able to reduce PitchBook seat counts after adopting platforms with bundled enrichment, though most still retain PitchBook for LCD-specific workflows. The consolidation question is firm-specific, but the exercise of asking it typically identifies at least one license that can be reduced or eliminated. Our data enrichment product page has more on how our bundled data works in practice.

The firms that treat enrichment as infrastructure will win

Private credit is growing faster than its data infrastructure. Firms that treat enrichment as a one-time cleanup project will keep reacting to stale data, missed covenants, and information gaps. Firms that build enrichment into the operating system will see borrower risks earlier, move faster on new opportunities, and deliver better outcomes to LPs.

The shift from periodic, manual enrichment to continuous, AI-native, waterfall enrichment is a strategic decision about how the firm operates, not a software decision about which CRM to buy. The firms that get this right will spend less time on data entry and more time on credit judgment, which is where returns actually come from.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Meridian is your team’s ultimate context provider, driving better deals while minimizing manual data entry.

What does data enrichment mean for private credit firms?

Data enrichment for private credit is the continuous process of enhancing CRM and portfolio records with verified information on borrower financials, credit risk, covenant compliance, and relationships. It is distinct from PE or VC enrichment because it requires ongoing monitoring of middle-market borrowers whose data is largely non-public.

What data enrichment works best for private credit CRMs?

Waterfall enrichment, where the CRM layers multiple data sources in a firm-controlled priority hierarchy with proprietary data on top, is the model that scales with portfolio complexity. AI-native enrichment that updates borrower profiles continuously outperforms any setup that depends on periodic manual imports.

How does waterfall data enrichment work?

The CRM checks data sources in a prioritized order: for each field on a borrower record, it pulls from Source A first, falls through to Source B for missing fields, supplements with Source C, and overlays the firm's own proprietary data as the top-priority layer. This approach shrinks coverage gaps because sources complement each other rather than overlap.

Which third-party data providers are best for private credit?

PitchBook covers deal and LCD data, Preqin covers fund and LP benchmarks, S&P Capital IQ covers ratings and covenants for larger borrowers, Dun & Bradstreet covers middle-market borrower creditworthiness, and Moody's Analytics covers probability-of-default modeling. No single provider covers the full universe, which is why most credit firms combine several in a waterfall.

What is the difference between AI-native enrichment and bolt-on AI?

AI-native enrichment is built into the platform's core architecture and actively maintains the underlying data layer. Bolt-on AI is a chatbot or copilot that queries data someone already entered manually, and cannot close data quality gaps on its own. For credit teams, the distinction matters because bolt-on AI cannot catch a covenant breach the underlying record does not reflect.

How much does a private credit data stack cost?

A comprehensive stack of PitchBook, Preqin, S&P Capital IQ, D&B, and a CRM can run well into six figures annually for a mid-size firm, with enterprise contracts going higher. This cost pressure is driving consolidation toward CRM platforms that bundle company and financial data directly, reducing the need for some standalone vendor subscriptions.

Table of Contents