Meridian MCP is live! Connect your deal sourcing data directly to Claude

Learn More

Meridian raises $7M seed round led by 645 Ventures.

Read More

Formatting documents still eats associate weekends. AI can now do it in minutes. Here's which tools handle each of the four core deal team documents — and why CRM-connected reporting wins long-term.

Private equity firms can now auto-generate formatted tear sheets and other presentation collateral from financial documents — but ask any associate at a private equity or venture firm what they actually did last weekend, and the answer hasn’t changed: they spent their weekend formatting documents. Built a tear sheet from a 60-page CIM. Pulled pipeline numbers into Excel. Compiled an IC memo from notes, emails, and a half-finished model. The work is critical, but very little of it is the work the team was hired to do; and it’s work AI can do now.

The reporting burden has grown alongside everything else in private markets: more deals, more data, more LP transparency requirements … but the same number of hours in a week. Yet most firms still produce tear sheets in PowerPoint, compile IC memos by copy-pasting from CIMs and data rooms, and build weekly pipeline reports by exporting from the CRM into a spreadsheet. The output is fine. The cost is in the calendar.

What has changed in the last 18 months is the architecture of the tools available to deal teams. AI-native CRMs now generate tear sheets from uploaded CIMs in minutes, draft IC memos from structured deal data and meeting transcripts, and build pipeline reports from live data without the export-and-format cycle. The documents that used to consume entire weekends can build themselves.

The shift matters because reporting is one of the few private markets workflows where the manual cost compounds with volume. A firm reviewing 200 CIMs a year and a firm reviewing 500 CIMs a year do not face proportional differences in deal team headcount; they face proportional differences in how much associate and VP time goes to formatting. The firms that compress that overhead earlier get to run thicker pipelines with the same team.

This guide covers the four document types that private markets deal teams produce most frequently, an architectural argument about why CRM-connected reporting compounds in value while standalone document tools do not, and an evaluation framework you can take into vendor conversations.

Almost every recurring document a deal team produces falls into one of four buckets. Each has a predictable structure, a predictable manual workflow, and a predictable failure mode when volume grows. We work through them in roughly the order a deal moves through the firm: tear sheet at intake, IC memo at decision, pipeline report on Monday morning, LP brief at quarter end.

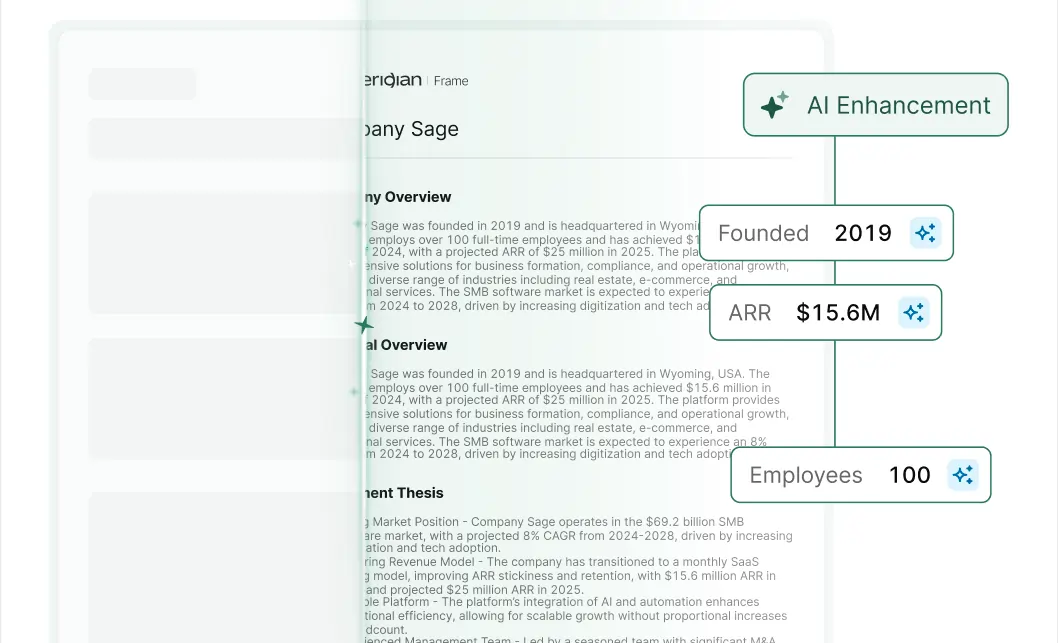

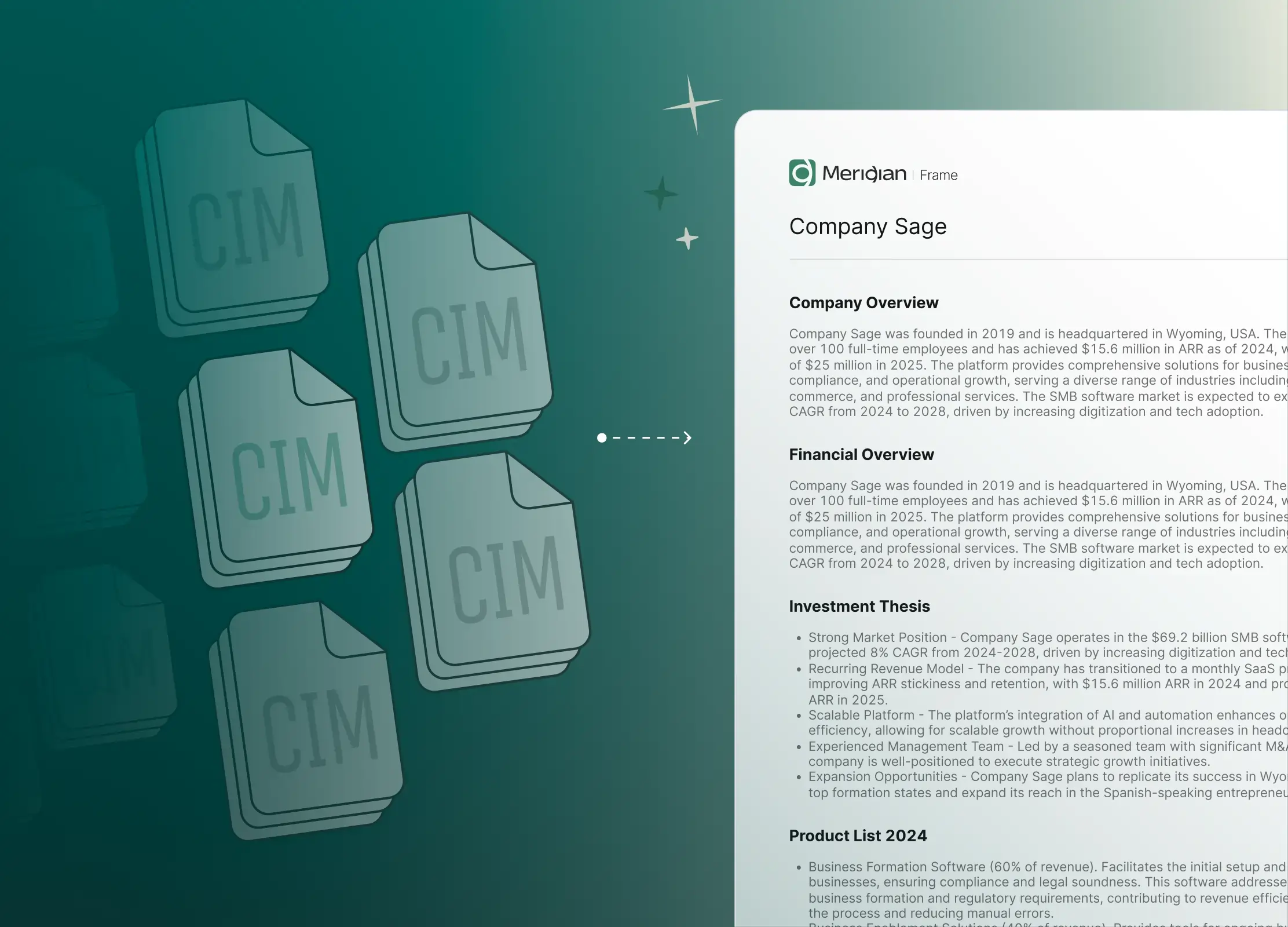

A tear sheet is a one or two-page summary of a company: headline financials, management team, deal history, sector context, and the investment angle. It is the document that decides whether a CIM gets a closer look or not. Tear sheets also show up in IC pre-reads, weekly pipeline meetings, and LP updates as portfolio summaries.

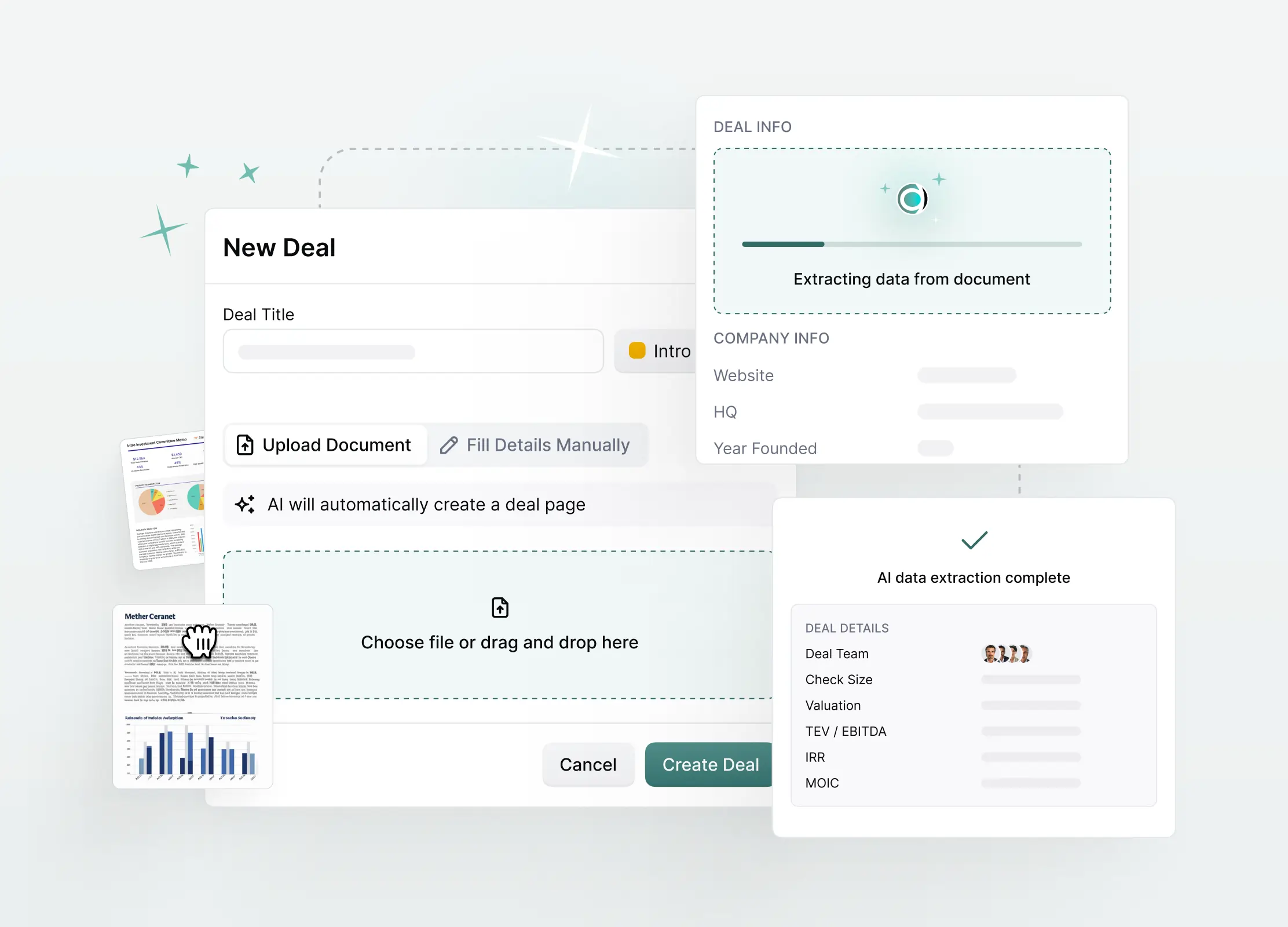

The manual workflow is the one every associate knows. A CIM lands in the inbox, somewhere between 40 and 120 pages. The associate reads it across two or three hours, pulls headline figures into a PowerPoint or Word template, cross-references with PitchBook or internal comps, formats the output, and sends it up. Total time per tear sheet: 2 to 4 hours, sometimes longer if the CIM is messy or the template is finicky.

The automated workflow inverts that ratio. Upload the CIM, the platform extracts key metrics, financial summaries, management bios, customer concentration, and risk factors, applies a template, and produces a branded summary. The associate's job shifts from extraction and formatting to review and judgment.

Meridian is built for this workflow. The platform converts CIMs and detailed decks into structured, accurate, branded investment summaries using firm-defined scoring criteria, with integrated deal scoring that runs against the firm's mandate. Meridian Frame works as a standalone extraction tool, but the output becomes richer when connected to the broader Meridian CRM: the tear sheet pulls in live firm data, prior deal evaluations, and enriched company profiles alongside the CIM-extracted content (press release).

Other tools cover this workflow from different angles. V7 Go's AI Tear Sheet Generation Agent extracts key metrics from CIMs, financial models, and management presentations, formats them to firm templates, and links every metric to its source page in the original document. V7 publishes a specific time contrast for the broader CIM to investment memo workflow: 5 to 7 hours manual versus 15 minutes with V7. V7 is a horizontal document-processing platform, so the tear sheet it produces sits outside the firm's CRM unless integrated separately.

Carta's tear sheet builder takes a different approach, pulling live fund economics (IRR, TVPI, DPI) directly into LP-facing tear sheets from Carta's fund administration data. This is the strongest option when the tear sheet is reporting fund performance to investors rather than evaluating a new company.

Allvue offers automated tear sheet generation tied to portfolio monitoring data, useful for firms that already run portfolio operations on Allvue.

For most deal teams, the tear sheet workflow is the highest-volume and highest-pain reporting task. It is also the easiest to compress. The input (a CIM) is structured enough for AI extraction, the output (a one-pager) is constrained enough to template, and the cost per document is high enough to justify a tool. Firms evaluating reporting automation should start here.

If the tear sheet is the document at intake, the IC memo is the document at decision. It is the comprehensive deal analysis presented to the investment committee: financial model summary, management assessment, market sizing, competitive landscape, risk factors, recommended deal terms. The package usually runs 15 to 40 pages with supporting exhibits, sometimes longer.

The manual workflow is the slowest in private markets reporting. Data gets pulled from CIMs, data rooms, meeting transcripts, external research, and prior deal comparables. An analyst and an associate spend one to two weeks compiling and formatting. There are multiple review rounds with the deal partner. Conflicting data points are reconciled by hand between sources. By the time it lands at IC, the team has spent more hours formatting than thinking.

The automated workflow does not eliminate the IC memo. Investment thesis, conviction, and critical analysis stay with the deal team. What automation removes is the assembly work: pulling CIM-extracted data into the right sections, surfacing relevant comparables from past deals, summarizing meeting transcripts with speaker attribution, and formatting market research into a usable structure. The senior team edits and adds judgment rather than starting from a blank page.

Meridian’s Scout AI sits at the center of this workflow inside the Meridian platform. Scout searches across deals, documents, emails, and prior IC decisions in natural language, so an associate preparing for IC can ask "What did we conclude on the last three healthcare services deals at this stage?" and get back relevant memo excerpts with citations. Meridian’s document extraction feature produces the tear sheet that anchors the IC package, and the CRM data that flows into both is the same data the deal team has been updating throughout diligence. The memo prep starts with everything the firm already knows.

Outside Meridian, several tools address pieces of the IC workflow. V7 Go's CIM analysis and investment memo agents handle the extraction and synthesis of deal documents, with every output cited back to source pages. Hebbia Matrix offers multi-agent document analysis for complex memo generation. Meeting capture tools like Jamie produce structured summaries with speaker attribution, useful as IC input when management presentations and diligence calls are the primary sources. Brownloop's Kairos platform is a consulting-led implementation of IC memo automation that has been deployed at a global PE firm with over $100 billion in AUM.

The pattern across these tools is consistent: AI handles the data assembly and the formatting, the deal team handles the judgment. The risk worth flagging is that a faster IC memo is only useful if the underlying analysis is still rigorous. Speed without conviction produces faster bad decisions. The right framing is that automation gives senior team members more time to argue about the deal and less time correcting the formatting on slide 14.

It is also worth being explicit about what should not be automated. The investment thesis, the read on the management team, the view on cyclical timing, the conviction on price discipline: these are the parts of the memo that pay the deal team's salary, and they do not improve when an LLM writes the first draft. The parts of the memo where automation pays off are the ones that consume time without testing judgment: comparable transactions tables, KPI extracts from the CIM, summaries of customer concentration, market sizing references, and prior internal commentary on the same sector. Teams that adopt automation well treat it as a way to compress the assembly work so that more meeting time goes to the parts that require argument.

For more on how the IC process is changing structurally, our take is in How the best firms run their investment committee.

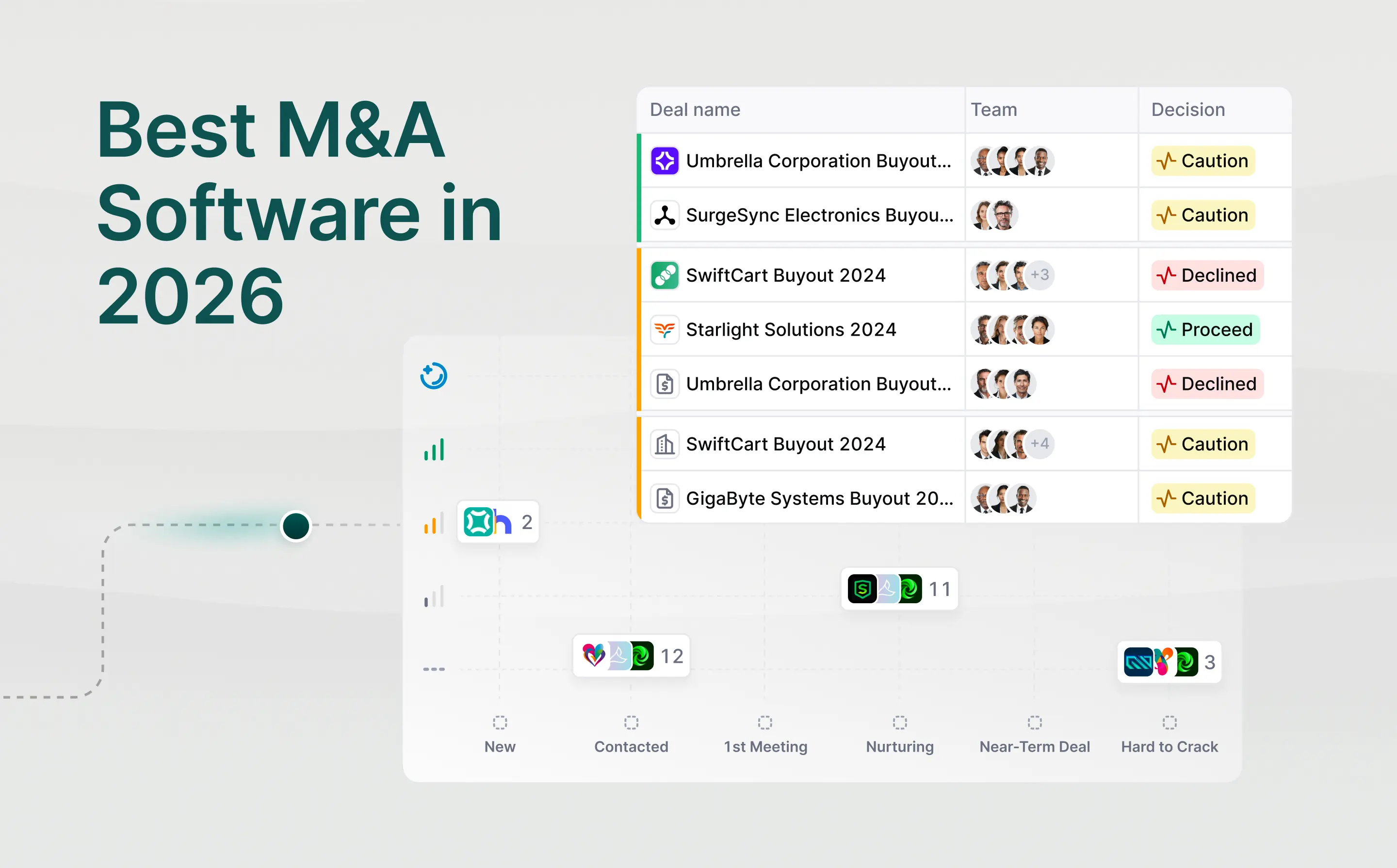

The Monday morning pipeline report is the document that most often gets built and least often gets read. It captures weekly pipeline status, team activity, sourcing analytics, deal-stage workload, and thematic coverage. It supports pipeline reviews, partner meetings, and resource allocation. It is also where the gap between what the CRM contains and what leadership sees becomes most obvious.

The manual workflow rarely scales. Someone in deal operations pulls a CRM export on Friday afternoon, formats charts and tables in Excel, emails the deck, and by Monday morning it is partially stale because deals moved over the weekend. If the firm uses a sales CRM not built for deal flow, the export usually requires custom views or SQL, which means deal ops becomes a bottleneck for the partner who wants to look at the data a different way.

The automated workflow makes pipeline reports a live surface rather than a static export. Filters run across deal stage, team member, sourcing theme, sector, time period, or any custom field, and the output renders in real time from the underlying CRM. Branded PDF and Excel exports are one click away when a static format is needed for a partner meeting or LP review. Natural-language queries replace the rebuild-the-dashboard cycle: A partner asks "Which thematic sectors generated the most IC-ready deals in the last six months, and which associates sourced them?" and gets back a chart-ready answer.

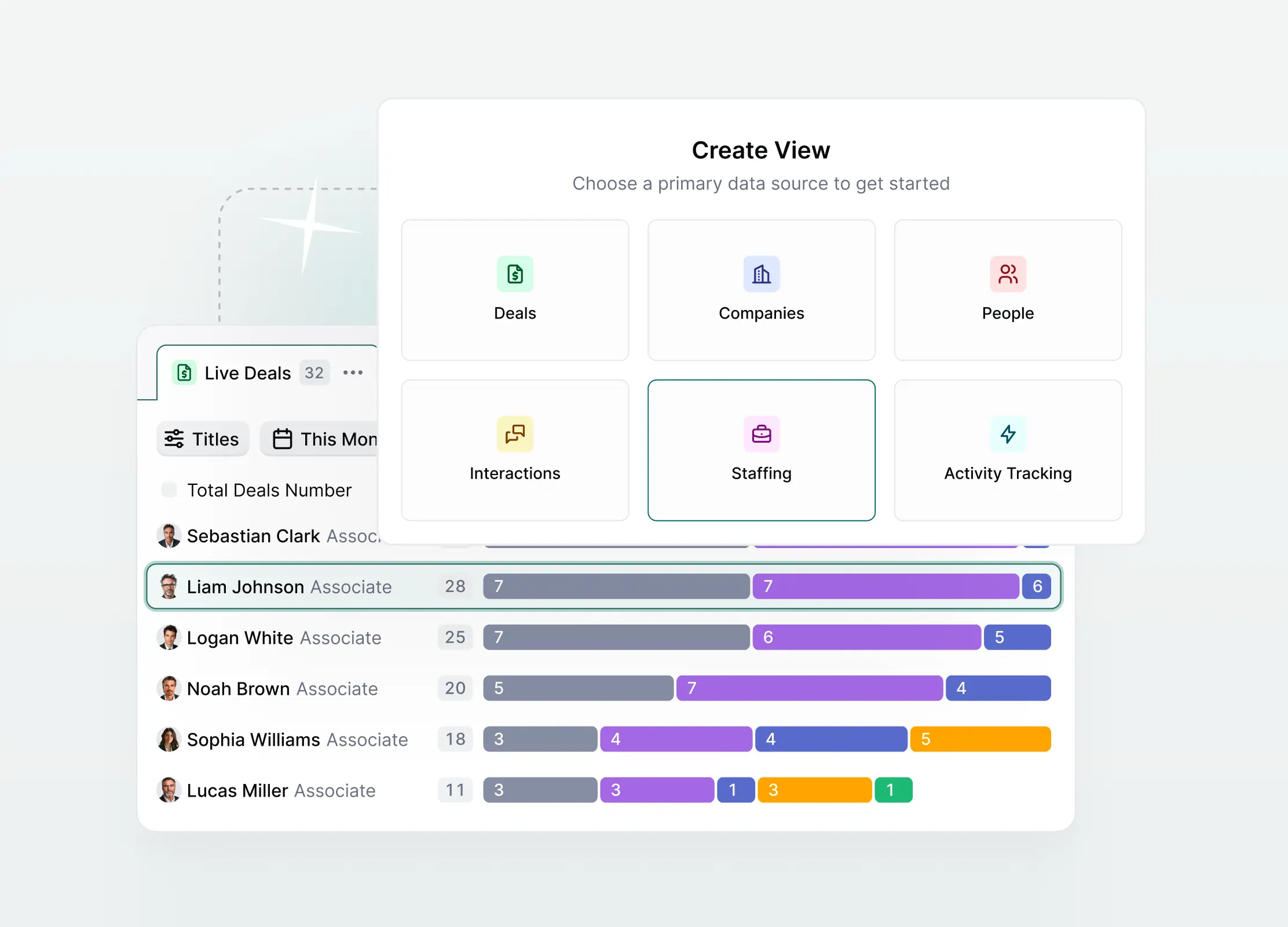

Inside Meridian, this work is split across several views that share the same underlying CRM data. The Reports module combines tab views into custom reports filterable across every CRM dimension. The Activity view shows team sourcing activity and engagement with follow-up gap detection. The Staffing view shows deal-stage workload across the team, which is the operational cockpit for a BD lead. The Interaction view shows relationship development at a glance, filtered by date, participants, company, or priority. Time-series views show how funnels, sourcing themes, or team activity have evolved over time. Every export carries the firm's branding.

Pipeline reporting is the document type where the architectural difference between CRM-connected and standalone tools matters most. A document-processing tool can produce a great tear sheet from a CIM, but it cannot tell you which sourcing channels are most productive this quarter or which associates have the highest IC-ready conversion rate. Those questions only have answers if the reporting tool is reading the same data the deal team updates every day. Our earlier piece on deal flow management covers this gap in more depth.

Meridian enables data-driven deal evaluation for smarter investment committee outcomes.

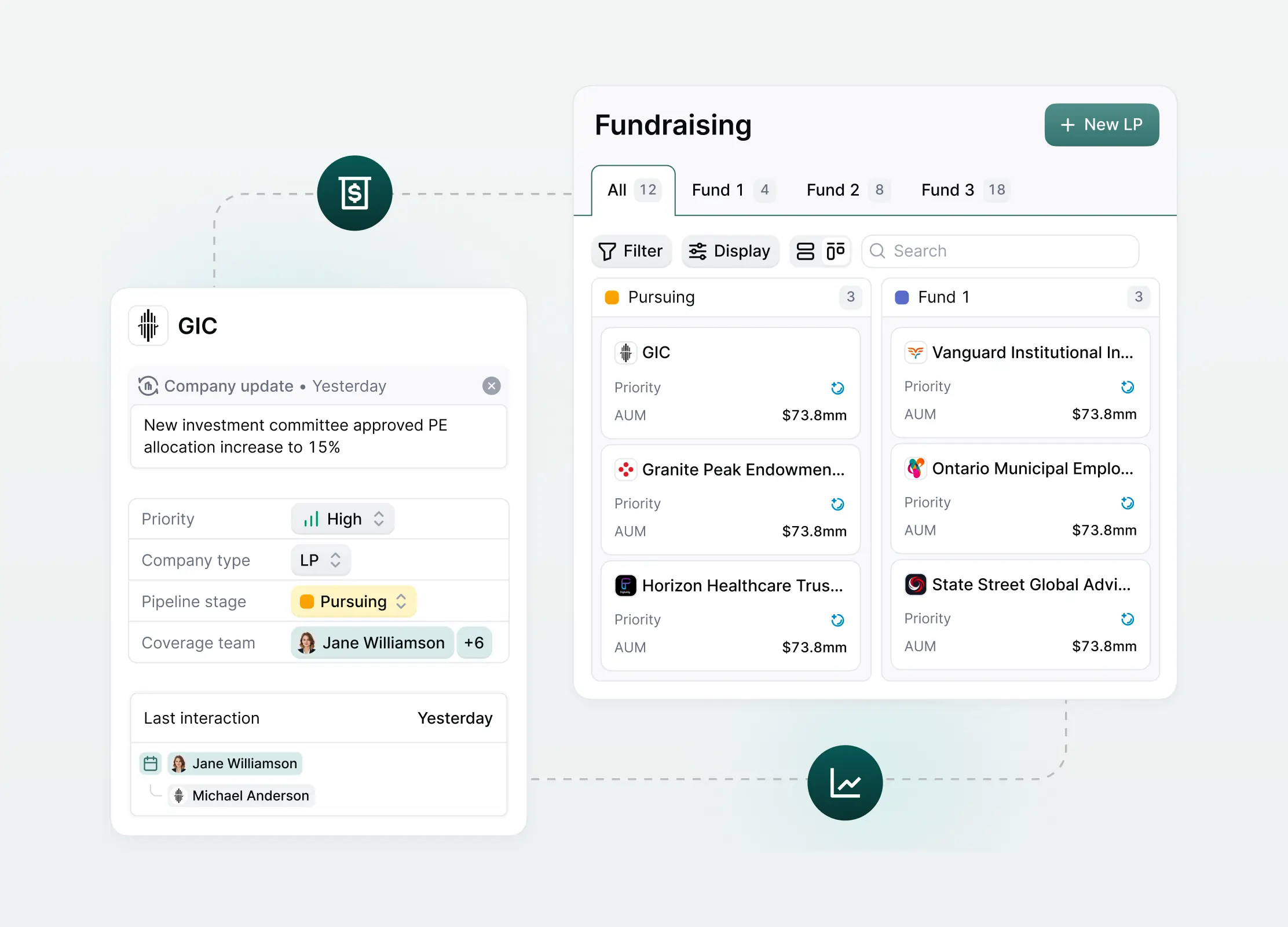

The fourth document type bridges deal activity and LP transparency. LP tear sheets, fund performance snapshots, commitment maps, and fundraising progress reports show up in quarterly letters, roadshow prep, and ad-hoc LP requests. They are the documents IR teams produce most often and that LPs scrutinize most carefully.

The manual workflow is fragmented because the underlying data sits in different systems. Performance data comes from fund administration. Deal status comes from the CRM. Market context comes from research. The IR team consolidates all of it in PowerPoint or Word, often a week of work for a single quarterly update. When LPs ask follow-up questions, the cycle restarts.

An automated workflow in a centralized system of record consolidates the inputs. When deal activity and LP data share a system, the CRM generates real-time LP summaries, commitment maps, and fundraising progress reports from live data. Tear sheets include structured metadata, activity logs, notes, and key context. One-click export to branded PDF or Excel makes the reports portable for the LP meeting. When deal data and LP data live in the same platform, the reports build themselves.

Meridian's fundraising and LP management module sits on top of the same CRM data the deal team uses. LP tear sheets reflect live pipeline activity. Commitment maps update automatically as documents close. Fundraising progress reports pull from the same interaction log that tracks every call and meeting. The IR team and the deal team work from one system rather than reconciling two.

Other tools cover specific slices of this workflow. Carta integrates fund economics directly into LP reporting, which is the strongest option for fund accounting metrics like IRR, TVPI, and DPI. Visible.vc is the most established tool for VC LP updates, with portfolio data collection built in and templates designed for the quarterly LP cycle. Allvue runs an investor portal with automated data feeds from fund administrators, useful for firms that already use Allvue for portfolio operations.

The honest trade-off for Meridian here is that we are a newer platform than Carta or Visible. Firms that have already invested in a fund-admin-first reporting stack will weigh that history. The argument in our favor is that LP reporting and deal flow have become structurally connected: LPs increasingly ask about pipeline composition, sourcing themes, and deal-stage velocity, not just realized returns. When those questions land in the IR team's inbox, the answers are easier to assemble from a CRM that already tracks them.

The reporting tool market splits cleanly into two architectures, and the choice between them shapes everything downstream.

Standalone document tools process uploaded documents in isolation. A CIM goes in, a structured output comes out. V7 Go, Hebbia, Frame, and similar platforms are powerful for one-off extraction and produce high-quality, source-cited outputs. Their limitation is that every document is a fresh starting point. The tear sheet they generate does not include the firm's prior evaluations of similar companies, the relationship history with the management team, or the enriched profile data the CRM has been accumulating. Each tear sheet is a snapshot of one CIM, not a synthesis of everything the firm knows about that opportunity.

CRM-connected reporting works the opposite way. The document is generated from the firm's living data, with the uploaded CIM as one input among many. A tear sheet includes CIM-extracted financials, but also the AI-generated deal score from enriched data, the relationship history with the management team, prior deals in the same sector, and any market signals the system has picked up. Pipeline reports pull from the same data the deal team updates daily, so the Monday morning view reflects the Friday evening state of the world. The documents are living outputs of the firm's operating system, not static artifacts.

The architectural argument cuts across the AI-native versus bolt-on debate that has shaped the broader CRM market. Intapp DealCloud's Celeste platform is the most visible example of bolt-on AI: a configurable database originally built in 2010, with an agentic AI layer added in 2026. Celeste is a credible product. The question worth asking is what data it is reasoning over. AI bolted onto a schema designed before AI existed inherits the constraints of that schema. AI-native platforms can structure their data, their workflows, and their UI for the AI layer from the start.

The same logic applies to reporting. Meridian's Scout is included with every seat and answers natural-language questions across deals, documents, emails, and IC decisions. The reporting features pull from the same data Scout reasons over, so the natural-language interface and the structured reports show the same view of the firm. There is no separate AI add-on to license, and no separate data layer for AI to query.

The open-architecture point is worth flagging. Meridian connects to Claude, ChatGPT, and external AI tools via MCP, APIs, and webhooks, which means the firm's CRM data is portable. If a better AI model emerges next year, the deal context still powers it. The firm's reporting capability is not tied to one vendor's model choices.

The compounding effect is the part that is easy to miss in a vendor demo. Standalone document tools produce one good tear sheet today and one good tear sheet next year, and the two outputs do not improve each other. CRM-connected platforms produce a tear sheet today that pulls from every prior tear sheet, every prior meeting note, and every prior IC discussion the firm has on file. The marginal output gets richer as the data accumulates. Two years of disciplined CRM use means the third year's reporting starts from a higher baseline than the first year's did, on the same software. That is the underlying argument for treating the CRM as the system of record rather than as one tool among several.

Vendor pitches collapse into a small set of architectural and operational criteria. The framework below covers the ones that matter most. We have kept Meridian out of this section deliberately: the criteria should hold whether you choose us or not.

CRM connectivity. Does the tool generate outputs from live CRM data, or does it process uploaded documents in isolation? CRM-connected tools produce richer outputs and stay current without manual effort. Standalone tools can be powerful for one-off extraction but require manual integration to stay aligned with the rest of the firm's data.

Document type coverage. Can the platform handle tear sheets, IC memos, pipeline reports, and LP briefs, or is it limited to one type? Single-purpose tools require multiple subscriptions and multiple workflows. The cost shows up in license fees and in the operational overhead of maintaining different templates across different systems.

Template flexibility. Can you customize output templates to match your firm's branding and formatting standards? White-labeled outputs matter most for LP-facing and partner-facing documents, but they also matter for internal credibility. A tear sheet that looks like a generic AI output undercuts the work that produced it.

AI query capability. Can you ask natural-language questions about your pipeline and get chart-ready answers, or is reporting limited to pre-built dashboards? The difference determines whether reporting is a periodic task scheduled into the calendar or an always-available resource that any team member can query when a question comes up.

Export formats. Does the tool export to branded PDF, Excel, and PowerPoint? IC packages often need to move across formats, and partner meetings often require a static deck. One-click export without formatting friction is the baseline expectation.

AI pricing model. Is AI reporting included in the platform or priced as a separate add-on? The architecture question and the pricing question are linked: platforms where AI is included tend to be the ones where AI was built in from the start, and platforms where AI is sold as a premium tier tend to be the ones where it was added later. Either model can work, but the buyer should know which they are getting.

Implementation timeline. How long from contract to live use across the firm? Reporting tools that require months of configuration before producing usable outputs lose half their value, because the firm's reporting needs change faster than the configuration cycle. Tools that work out of the box for private markets workflows compress this gap.

The best deal teams in 2026 do not "do reporting." Their CRM does reporting for them. Tear sheets generate from uploaded CIMs. Pipeline reports build from live data. IC packages assemble from enriched profiles and meeting transcripts. LP briefs pull from the same system that tracks deals. When reporting is a byproduct of how the team already works, the hours associates and VPs spent formatting documents go back to evaluating deals.

The choice of reporting tool is downstream of a more fundamental question: Where does your firm's operating data live, and what does the AI layer get to reason over? Standalone tools can produce excellent documents from individual files. CRM-connected platforms produce documents that compound in value as the firm accumulates context. Both have a place in the market. The decision worth making deliberately is which one anchors the workflow.

Discover how Meridian can streamline deal sourcing and enhance your decision-making

Meridian was built by and for PE professionals, providing tools that keep your firm strategic, efficient, and ahead of the game.

Upload the CIM into a tear sheet automation tool, the platform extracts financials, management information, and risk factors, applies a firm-defined template, and produces a branded one-pager. Meridian runs this workflow with integrated deal scoring against the firm's mandate. Carta's tear sheet builder handles the same workflow when the input is fund performance data rather than a deal CIM.

A CRM cannot replace the investment thesis or the critical analysis that belongs in an IC memo, but it can assemble the structured inputs the memo depends on. Meridian Scout searches across deals, documents, emails, and prior IC decisions in natural language, so memo prep starts from the firm's accumulated context rather than a blank page. The deal team adds the judgment.

The main options split between CRM-connected platforms and standalone document tools. Meridian Frame and Carta sit in the CRM-connected category. V7 Go, Hebbia, and similar tools sit in the standalone category. The distinction matters because CRM-connected outputs include firm context that standalone outputs cannot.

Most AI tear sheet tools produce a structured output in minutes, compared to 2 to 4 hours for the equivalent manual workflow. V7 publishes a specific contrast for the broader CIM to investment memo process of 5 to 7 hours manual versus 15 minutes with AI extraction. The variance depends on CIM complexity and template customization.

Built-in AI shares the same data model and the same UI as the rest of the platform, so reporting, search, and document generation all read from one source. Bolted-on AI is added as a separate layer over an existing database, which can deliver capable features but inherits the schema and the constraints of the underlying system. Intapp's DealCloud with Celeste is an example of bolted-on AI; Meridian Scout is an example of built-in AI. Both models can produce useful outputs. The architectural difference shows up most clearly when users want to query across all of the firm's data in natural language.

Modern private markets reporting platforms support one-click export to branded PDF, Excel, and PowerPoint formats without manual reformatting. This is the baseline expectation for any tool used in LP-facing or partner-facing workflows. Tools that require post-export cleanup in PowerPoint should be evaluated carefully.

At minimum: dynamic pipeline reporting with filterable views, an activity view for team sourcing engagement, a staffing or workload view for deal-stage allocation, an interaction view for relationship development, time-series analysis for funnel and theme evolution, natural-language AI queries against the underlying data, and one-click branded export. The best private equity CRM tools in 2026 ship most of these out of the box; legacy tools generally do not.

Table of Contents

Why most investment firm CRM rollouts fail, and the five criteria plus 90-day process that predict which platforms actually get used.